THE UNITED REPUBLIC OF TANZANIA, PRIME MINISTER'S OFFICE REGIONAL ADMINISTRATION AND LOCAL GOVERNMENT

FORM THREE TERMINAL EXAMINATIONS

062 BOOK KEEPING

Time 3:00 HRS May, 2026

INSTRUCTIONS

- This paper consists of section A, B and C with a total of nine (9) questions.

- Answer all questions in section A, B and C.

- Section A carries fifteen (15) marks, section B carries forty (40) marks and C carries forty-five (45) marks.

- Non programmable calculators may be used.

- Communication devices and any unauthorized materials are not allowed in the examination room.

- Write your examination number on every page of your answer booklet (s).

SECTION A (15 marks)

Answer all questions

1. For each of the items (i) - (x) choose the correct answer from the given alternatives and write its letter beside the item number of the correct answer in the box provided.

i) One of the following describe meaning of capital expenditure:

- Extra capital paid n by the proprietor

- The extra purchase of goods for sale

- The cost of running the business on a day-to-day basis

- Money spent on buying fixed assets or adding value to them

- Money spent as revenue expenditure

ii) When the financial statement is prepared, the Bad debts Account is closed by transfer to the;-

- Income Statement,

- Statement of financial position,

- Debtor’s personal account

- Provision for doubtful Debts Account

- Trading account

iii) In the trial balance, the balance on the provision for Doubtful debts Account is;-

- Shown as a credit item,

- Not shown,

- Shown as a debit item,

- Sometimes debit, sometimes credit.

- Shown as bad debts.

iv) An invoice shown a total of shs 3200/= less 2.5% cash discount. If this was paid in time, the Amount of the cheque paid would be for;-

- T.Shs 2960

- T.Shs 3040

- T.Shs 3120

- T.Shs 2800

- T.shs 3280

v) Given an opening capital of TZS 500,000, Closing capital of TZS 1,800,000 and drawings for the year of TZS 200,000: How much would be the profit or loss for the year?

- Loss for the year is TZS 1,000,000

- Loss for the year is TZS 2,100,000

- Profit for the year is TZS 2,500,000

- Loss for the year is TZS 1,100,000

- Profit for the year is TZS 1,500,000

vi) Which item would not be considered in the process of preparing Receipts and Payments account for the religious organization?

- Cheque paid during the year

- Subscription received

- Surplus

- Bank balance

- Receipts from sales of an assets

vii) A sole trader started business with cash from her savings of TZS 1,000,000, and equipment valued TZS 200,000, motor van valued TZS 2,000,000 and a loan from Upendo SACCOS TZS 300,000. How much would be a capital of a sole trader?

- TZS 1,200,000

- TZS 3,500,000

- TZS 2,900,000

- TZS 2,200,000

- TZS 3,200,000

viii) Which of the following would be entered in the journal?

- Payment for cash purchases

- Fixture bought for cash

- Credit sales of goods

- Sales of surplus machinery

- Goods sold for cash

ix) Errors are corrected through the journal because:

- It saves the book-keepers time

- It saves entering them in the ledger

- It is much easier to record entries in the journal

- It shows assets in the credit side and liabilities in the debit side

- It provides a good record explaining the double entry system.

x) Which of the following is liability?

- Loan from J John

- Building

- Accounts receivable

- Work in progress at the end

- Closing stock of finished goods

2. Match the items in Column A with the responses in Column B by writing the letter of the correct response below the corresponding item number in the table provided.

| COLUMN A | COLUMN B |

| (i) Concepts requires every financial transaction to be recorded in at least two different accounts (ii) States that enterprises prepare its books of account assuming that the business will continue to operate in the foreseeable future (iii) Require ana assets to be recorded in the books of accounts and presented on the financial position at their original cost. (iv) Requires an enterprise to match revenues and their related expenses in the same accounting period in the process of determining a profit or loss. (v) It requires that the life of business is divided into uniform time intervals. |

|

SECTION B (40 marks)

Answer all questions in this section

3. (a) Describe two (02) difference between capital expenditure and revenue expenditure.

(b) Some of the following items should be treated as capital expenditure and some as revenue expenditure. For each of them state which classification applies:

- The purchase petrol for generator for use in the business . . . . . . . . . . . . . . . . .

- Carriage paid stocks sold in the business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

- Complete construction of the premises at cost of 150 millions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

- Payment made for a buying stationery . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

- The purchase of a bricks and others construction materials for new office . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4. (a) Describe the meaning of the Books of Prime entry.

(b) Books of prime entry are also known as books of original entry or subsidiary books. As an expert explain six (6) types of books of prime entry.

5. DOLY estate extracted a trial balance from is book- keeping records on 30th June 2024. The trial balance failed to agree and the difference was TZS 247,000, a shortage on the debit side. This was placed to a suspense account pending further investigation. The following errors were later found:

- A TZS 1,105,000 cheque payment for general expenses had been entered in the cash book but no entry had been made in the general expenses account.

- A cheque payment for wages TZS 1,131,000 had been correctly entered in the cash book but was entered as TZS 1,031,000 in the wages account

- (iii)Commission received of TZS 325,000 had been entered twice in the commission income account

- A cheque payment for telephone expenses TZS 624,000 had been debited to both the telephone expenses account and the bank account

- Stationaries expenses TZS 715,000 had not been entered in the stationaries expenses account to correct the errors.

Enter the above transactions in the general journal (ignore narrations) and post to the suspense account to correct the errors.

6) (a) Cash book is a book used to record movement of cash into the business and out of the business. Identify four types of cash book

(b) Monica opened a new business dealing with second hand clothes on a whole sale basis. She started the business on 1st July 2021 with a capital of TZS 40,000,000 in cash.

| TZS | |

| July 1 paid cash for six months’ rent of the shop | 900,000 |

| July 2 bought clothes in cash | 16,500,000 |

| July 2 paid transport charges in cash | 120,000 |

| July 3 bought packaging materials in cash | 80,000 |

| July 6 sold clothes in cash | 7,200,000 |

| July 8 purchased clothes in cash | 4,800,000 |

| July 15 paid wages and commission in cash | 1,200,000 |

| July 18 cash sales | 15,200,000 |

| July 22 cash purchases | 5,400,000 |

| July 25 cash sales | 10,000,000 |

| July 26 paid for stationaries in cash | 200,000 |

Required :

Enter the above transactions in a cash account and balance the account as at 31st July 2021

SECTION (C 45 marks)

Answer all questions in this section

7. From the following information prepare the sales ledger control account for the month of August 2012.

| TZS | |

| August 1 sales ledger – debit balance | 381,600 |

| 1 sales ledger -credit balance | 2,200 |

| 31st Transactions for the month: | |

| Cash received | 10,400 |

| Cheque received | 623,900 |

| Bill received | 300,000 |

| Sales | 709,000 |

| Bad debts written off | 30,600 |

| Discount allowed | 29,800 |

| Returns inwards | 66,400 |

| Cash refunded to the customers who had over paid | 3,700 |

| Dishonored cheque | 2,900 |

8. A company depreciates its plant at the rate of 25% per annum, straight line method, for each month of ownership. From the following details draw up the plant account and the provision for depreciation account for each of the years 2004, 2005,2006 and 2007.

- 2004 bought plant costing TZS 2,600 on 1st January.

- Bought plant costing TZS 2,100 on 1st October.

- 2006 bought plant costing TZS 2,800 on 1st September.

- 2007 sold plant which had been bought for TZS 2,600 on 1st January 2004 for the sum of TZS 810 on 31st august 2007

You are also required to draw up the plant disposal account.

9. From the following Trial balance of Erick Brown , store owner Prepare the Income statement for the year ended 31st December 2007, and a Statement of Financial Position as at 31st December 2007, taking into consideration the adjustments shown below:

Trial balance as at 31st December 2007:

| PARTICULARS | DR (TZS) | CR (TZS) |

| Sales | 400,000 | |

| Purchases | 350,000 | |

| Sales returns | 5,000 | |

| Purchases returns | 6,200 | |

| Opening stock at 1st January 2007 | 100,000 | |

| Provision for doubtful debts | 800 | |

| Wages and salaries | 30,000 | |

| Rates | 6,000 | |

| Telephones | 1,000 | |

| Shop fittings at cost | 40,000 | |

| Van at cost | 30,000 | |

| Debtors and creditors | 9,800 | 7,000 |

| Bad debts | 200 | |

| Capital | 179,000 | |

| Bank balance | 3,000 | |

| Drawings | 18,000 | |

| Total | 593,000 | 593,000 |

Additional information:

- Closing stock at 31st December 2007 TZS 120,000

- Accrued wages TZS 5,000

- Rates prepaid TZS 500

- The provision for doubtful debts to be increased to 10 per cent of debtors

- Telephone account outstanding TZS 220

- Depreciation shop fittings at 10 per cent per annum, and van at 20 per cent per annum on cost

FORM THREE BKEEPING EXAM SERIES 263

FORM THREE BKEEPING EXAM SERIES 263

PRESIDENT'S OFFICE REGIONAL ADMINISTRATION AND LOCAL GOVERNMENT

FORM THREE ANNUAL EXAMINATION

062 BOOK KEEPING

TIME: 3:00 Hours November, 2025

INSTRUCTIONS

- Answer all question in section A, B, and C.

- Show your working clearly

SECTION A:

Answer all questions in this section

1. Choose the correct answer and write its letter in the box provided.

i. Who is a Paymaster General (PMG) of The United Republic of Tanzania?

- The shadow minister of the ministry of planning and finance.

- Controller and Auditor General (CAG).

- The minister of the ministry planning and finance.

- The permanent secretary of the ministry of planning and finance.

- The permanent secretary

ii. When a petty cash book is kept there will be;

- More entries will be made in the cash book.

- More entries made in the general ledger

- Fewer entries made in the general ledger

- The same number of entries in the general ledger

- No entries made at all in the general ledger for items paid by petty cash.

iii. When the final accounts are prepared, the Bad Debts Account is closed by a transfer to the;

- Balance Sheet.

- Profit and Loss Account.

- Cash flow statement. Debts Account

- Trading Account.

- Provision for Doubtful

iv. Overlooking an item of stock costing TZS. 1,000 (selling price TZS. 1,500) during the yearend stocktaking would result in:

- Overstating Gross Profit by TZS. 1,500.

- Overstating Current Assets by TZS. 1,500.

- Understating Gross Profit by TZS. 1,000.

- Overstating Gross Profit by TZS. 1,000.

- Overstating net profit by TZS. 1,500

v. The total of the ‘Discounts Allowed’ column in the Cash Book is posted to;

- The debit side of cash account.

- The debit of the Discounts Allowed account

- The debit of the Discounts Received account.

- The credit of the Discounts Allowed account.

- The credit of the Discounts Received account

vi. CHEQUE which is not accepted for payment by the bank due to insufficient fund in the drawer’s bank account is known as;

- Staled CHEQUE.

- Un-credited CHEQUE.

- Dirty CHEQUE.

- Un-presented CHEQUE.

- Dishonored CHEQUE

vii. Which of the following is a revenue expenditure associated with a motor vehicle?

- Motor vehicles account

- Carriage inwards costs of a motor vehicle

- Motor vehicles running costs

- Import duties for a new motor vehicle

- Wages to a driver who brought a motor vehicle to the business

viii. Company paid in advance TZS. 48,000 for two years insurance which started on 1st May 2016 and recorded the whole amount as an asset. The adjusting entry on fiscal year ended 31st December 2016 of that year is;

- Debit insurance expenses; credit prepaid insurance TZS. 12,000.

- Debit insurance expenses; credit prepaid insurance TZS. 8,000.

- Debit prepaid insurance expenses; credit insurance expenses TZS. 16,000.

- Debit insurance expenses; credit prepaid insurance TZS. 16,000.

- Debit insurance expenses; credit cash book TZS. 16,000.

ix. What should happen if the balance on a Suspense Account is of a material amount?

- Should be written off to the balance sheet.

- Carry forward the balance to the next period.

- Find the error(s) before publishing the final accounts.

- Write it off to Profit and Loss Account.

- Write-off the amount through profit or loss.

x. Basic rule of double-entry bookkeeping is;

- Every debit entry must be matched by another debit entry.

- Debit the giver and credit the receiver.

- Every credit entry must be matched by another credit entry.

- Debt the receiver and credit the giver.

- Every transaction to be recorded twice.

2. Match the items in Column A with the responses in Column B by writing the letter of the correct response in the answer sheets provided.

| Column A | Column B |

|

|

SECTION B:

Answer all question in this section

3. Mtumba confused when his cash book and bank statement balance disagree on 31 December 2007 the following are details found which lead to that problem

- Cash at bank as per bank column of the cash book 16,000/=

- Unpresented cheques 3,500 /=

- Cheques received and paid into the bank, but not yet entered on the bank statement 3,950 /= Bank charges 1,350/=

- Credit transfers entered as banked on the bank statement but not entered in the cash book 3,700/=

- Cash at bank as per bank statement 17,900

Prepare the bank reconciliation statement as at 31st December 2024

4. Nunda Kimti his trial balances total amount did not match. You as expert of bookkeeping correct the errors below by showing the entry on journal (narration not necessary)

- Extra capital of Tshs. 5,000 paid into the bank had been credited to Sales account.

- Goods taken for own use Tshs 72,000/= had been debited to Sundry Expenses.

- Private rent Tshs 2,300/= had been debited to the Rent account.

- A purchase of goods from D Pine Tshs 3,990/= had been entered in the books as Tshs 4,790/=

5. Kiumbe Katoto made the payment of different activities on behalf of his Accountant.. as commerce student help Mr. Katoto to arrange that payment in the types of the as shown in the table below.

| BUSINESS EVENTS | TYPE OF EXPENDITURE | |

| I | Electricity costs of using machinery | |

| II | The cost of acquiring patent rights. | |

| III | Painting outside of new building | |

| IV | A motor vehicle bought for re-sale by a motor dealer. | |

| V | Twelve dozen sets of cutlery, purchased by a cateringfirm for a new dining-room. | |

| VI | Cost of hiring refrigeration plant in a butcher’s shop. | |

| VII | The cost of installing a new machine. | |

| VIII | Repairs to a fritterers’ van. | |

| IX | Break-down van purchased by a garage | |

| X | Petrol costs for van |

6. Mr. Mpita his stock was stolen on 1 June 2001. The last time that a stock-taking had been done was on 31 December 2000, the last balance sheet date, when stock was valued at cost at Tshs.20,000/=. Purchases from then until 1 June 2001 amounted to Tshs 138,000/= and sales in that period were Tshs.165,500/=. The gross profit of his business often is 15 percent of sales . As his friends help him to determine the cost of goods stolen.

SECTION C: Answer all questions on this section

7. Sikitu Ltd provides for depreciation of its machinery at 20% per annum on cost; it charges for a full year in the year of purchase but no provision is made in the year of sale/disposal.

Financial statements are prepared annually to 31 December.

2001

- January 1 Bought machine ‘A’ Tshs 10,000 July 1 Bought machine ‘B’ Tshs 6,000.

2002

- March 31 Bought machine ‘C’ Tshs 8,000

2003

- October 7 Sold machine ‘A’ – proceeds Tshs 5,500

- November 5 Bought machine ‘D’ Tshs 12,000

2004

- February 4 Sold machine ‘B’ – proceedsTshs3,000

- February 6 Bought machine ‘B’ Tshs 9,000

- October 11 Exchanged machine ‘D’ for a motor vehicle valued atTshs7,000

Prepare

- The accumulated provision for depreciation on machinery account, for the period 1st January2001 to 31st December 2004

- The disposal of machinery accounts showing the profit/loss on sale for each year.

8. From the following figures, compile account receivable ledger and account payable ledger control accounts for the month, and ascertain what the net balances of the respective ledgers should be on 31 January 2010.

Balances on 1 January 2010 Tshs

- Debtors ledger – Dr 139,386

- Debtors ledger–Cr 735

- Creditors ledger – Dr 4,416

- Creditors ledger –Cr 76,395

Total for the month to 31 January 2010

- Purchases 229,422

- Sales 378,072

- Purchase returns 6,462

- Sales returns 11,000

- Debtors accounts settled by contra accounts with creditors 1,365

- Bad debt written off 3,759

- Discounts and allowances to customers 2,238

- Cash received from customers 350,392

- Cash discount received 5,826

- Cash paid to creditors 211,428

- Cash paid to customers 156

9. The following trial balance was extracted from the books of Free Dodo Shop at the close of business on 28 February 2012.

|

| Dr Tshs | Cr Tshs |

| Purchases and sales | 371,200 | 628,660 |

| Cash at bank | 16,400 | |

| Cash in hand | 324 | |

| Capital account 1 March 2011 | 45,600 | |

| Drawings | 68,400 | |

| Office furniture | 11,600 | |

| Rent | 13,600 | |

| Wages and salaries | 125,600 | |

| Discounts | 3,280 | 640 |

| Debtors and creditors | 49,264 | 20,980 |

| Inventories 1 March 2011 | 16,480 | |

| Provision for doubtful debts 1 March 2011 | 1,620 | |

| Delivery van | 15,000 | |

| Van running costs | 2,480 | |

| Bad debts written off | 2,920 | |

| 697,500 | 697,500 |

Other information

- Inventories 28 February 2012 Tshs 9,600.

- Wages and salaries accrued at 28 February 2012 Tshs 13600.

- Rent prepaid at 28 February 2012 Tshs 920.

- Van running costs owing at 28 February 2012 Tshs 288.

- Increase the provision for doubtful debts by Tshs 364.

- Provide for depreciation as follows: Office furniture Tshs 1520; Delivery van Tshs 5,000.

Required:

- Prepare the income statement for the year ending 28 February 2012 together with a statement of financial position as on 28 February 2012.

FORM THREE BKEEPING EXAM SERIES 251

FORM THREE BKEEPING EXAM SERIES 251

FORM THREE BKEEPING EXAM SERIES 216

FORM THREE BKEEPING EXAM SERIES 216

FORM THREE BKEEPING EXAM SERIES 204

FORM THREE BKEEPING EXAM SERIES 204

THE UNITED REPUBLIC OF TANZANIA PRESIDENT’S OFFICE

REGIONAL ADMINISTRATION AND LOCAL GOVERNMENT

FORM TREE MID TERM TEST MARCH-2025

033/1 BOOK-KEEPING

Time: 3 Hours MARCH, 2025

Instructions

- This paper consists of three sections A, B and C with a total of 9 questions.

- Answer all questions in section A and B and only two (2) questions from section C.

- Section A carries twenty (20) marks, section B forty (40) marks and section C forty (40) marks.

- Non programmable calculators may be used.

- Cellular phones, and other authorized materials are not allowed in the examination room.

- Write your examination number on every page of your Answer booklet(s).

SECTION A (20 MARKS)

Answer all questions in this section

1. For each of the items (i)-(xv), choose the correct answer from among the given

Alternatives and write its letter beside the item number in the answer sheet provided

- If sales is 20,000 and profit make up is 25%, determine the amount of cost price

- 13,600

- 12,000

- 16,000

- 12,900

- 20,600

- Which book of prime entry records the sale or purchase of non-current Assets?

- General journal

- Sales journal

- Purchases journal

- Cash book

- Sales return day book

- If cash sale amount to Tshs 100,000/= paid direct into the bank account, the correct double entry will be to

- Debit sales account and credit cash account by sh.100, 000

- Debit cash account and credit bank account by sh.100, 000

- Debit bank account and credit sales account by sh.100, 000

- Debit bank account and credit cash account by sh.100, 000

- Debit sales account and credit bank account by sh.100, 000

- How much is to be reimbursed if a petty cashier has spent Tsh.189,00/=while his cash float is Tsh.200,000/=

- Tsh,11,000/=

- Tsh 389,000/=

- Tsh,189,000/=

- Tsh,200,000/=

- Tsh,21,000/=

- Working capital is a term meaning.

- The excess of current liabilities over current liabilities

- The excess of the current assets over the current liabilities

- the excess of the current assets over non-current liabilities

- The excess of current assets over non-current assets.

- The excess of non-current Assets over current liabilities

- Natasha and Ndengwe share profits and losses in the ratio 3:2. Their partnership recorded net profits of shs. 1,400, interest on capital shs. 420, partners’ salaries shs. 100 and drawings shs. 280, Determine Ndengwe’s share of the profits.

- TZS 840

- TZS 560

- TZS 464

- TZS 696

- TZS 506

- From the following categories of errors, identify the category of errors which affect only one account

- Casting errors

- Errors of principle

- Errors of omission.

- Errors of original entry.

- Errors of commission.

- In the business of C. Sangster, who owns a clothing store, which of the following is the capital expenditure?

- Fixtures and New Van bought

- Shop fixtures bought and wages of assistants

- Wages of assistants and new van bought

- Wages of assistants and Petrol for Van

- Fixtures and salaries.

- Manufacturing account is used to calculate:

- Production cost paid in the year

- Total cost of goods produced

- Production cost of goods completed

- Gross profit on goods sold

- Prime cost of goods manufactured

- Depreciation can be described as the : _______

- Amount spent to buy a non –current asset

- Salvage value of a non-current asset consumed during its period

- Cost of the non-current asset consumed during its period

- Amount of money spent replacing non-current asset

- Cost of old asset plus new assets purchased

- A bank reconciliation statement is a statement:

- Sent by bank when the account are overdrawn

- Drawn to verify cash book balance with the bank statement balance

- Drawn up by the bank to verify the cash book

- Sent by the bank to the customers when errors are made

- Sent by the bank customers to the friends.

- If two totals of trial balance do not agree, the difference must be entered in:

- A real account

- The trading accounts

- A nominal account

- The capital account

- A suspense account

- The accounting equation is expressed in the financial statement called:

- statement of financial position

- income statement

- expenditure statement

- reconciliation statement

- statement of change in equity

- If we take goods for own use, we should

- Debit drawings Account: Credit Purchase Account

- Debit Purchases Account: Credit Drawings Account

- Debit Drawings Account: Credit Inventory Account

- Debit Sales Account: Credit Inventory account

- debit inventory Account: Credit Drawing Account

- if a partnership maintains a fixed capital account, then the partner’s share

of profits is:

- Credited to the partner’s drawings account

- debited to the partner’s capital account

- credited to the partner’s capital account

- credited to the partner’s current account

- debited to the partner’s current account

2. For each of the items (i)-( v) match the narrations of bank reconciliation Items in column A with their corresponding names in column B by writing the letter of the correct response beside the item number in the answer sheet provided

| COLUMN A | COLUMN B |

|

|

SECTION B (40 MARKS)

Answer all questions in this section.

3. In 1991 Mr. Chipepeto bought a motor car for the cost value of sh.8, 000,000/= with the aim of assisting him in business. But three years later he decided to dispose it for a book value of sh.6,700,000/=

- What is the term used to mean the difference between cost value and book value.

- Outline four reasons that could be the causes for him to dispose the car for less than the cost value.

4. The DSM Rotary club, has provided you with the following information:-

| As at 31st December | 2000 | 2001 |

| Subscription in arrears | 6400 | 8800 |

| Subscription in advance | 1200 | 3400 |

| Subscription during the year | - | 20,200 |

| Insurance expenses owing (in arrears) | 3700 | 2700 |

| Insurance expenses prepaid (in advance) | 4400 | 5200 |

| Insurance paid during the year | - | 16,800 |

Required: Prepare A Subscription account and Insurance account, clearly showing amounts to be transferred to income and expenditure accounts for year 2001.

5. Define the following terms

- Discount received

- Invoice

- Discount allowed

- Carriage inwards

- Carriage outwards

6. (a) Mr. Kyamba wants to start a business, but before commencement he needs to learn book keeping. Outline five objectives for him to study book keeping.

(b) Briefly explain three types of a cash book.

SECTION C (40 MARKS)

Answer two questions only from this section.

7. Panguso& company limited own a manufacturing industry which had the following records for the year ended at 31st December 2007.

- Inventory at 1st January 2007:

- raw materials sh.760, 000

- Finished goods sh 360,000

- Purchases of raw material sh.420, 000

- Sales of finished goods sh.2, 490,000

- Factory Fuel & power sh.320, 000

- Royalty sh.500, 000

- Depreciation of works machine sh.88, 000

- Market value sh.1,800,670

- General office expense sh.10, 740

- Manufacturing wages sh.170, 000

- Inventory at 31 stDec 2007: raw material sh.900, 000

- Finished goods sh.580, 000

- Works in progress sh.734, 000

You are required to prepare

- Statement of manufacturing costs for the year ended at 31 stDec 2007

- Income statement for the year ended at 31.12.2007

8. XY Ltd provides for depreciation of its machinery at 20% per annum on cost; it charges for a full year in the year of purchase but no provision is made in year of sale/disposal.

Financial statements are prepared annually to 31th December. 2015

- January 1 Bought machine ‘A’ 10,000

- July 1 Bought machine ‘B’ 6,000

2016

- March 31 Bought machine ‘B’ 8,000

2017

- October 7 Sold machine ‘A’ – proceeds 5,500

- November 5 Bought machine ‘D’ 12,000

2018

- February 4 Sold machine ‘B’ – proceeds 3,000

- February 6 Bought machine ‘B’ 9,000

- October 11 Exchanged machine ‘D’ for machine valued at 7,000

Prepare;

- The machinery account for the period 1st January 2015 to 31st December 2018

- The accumulated provision for depreciation on machinery account, for the period 1st January 2015 to 31st December 2018.

9. The financial of the GGM trading company ended on 30th November 2014. You have been asked to prepare a total amount receivable and total amount payable for the draft final amounts. You are able to obtain the following information for the financial year the book of original entry.

| Sales | – Cash 344,890 – Credit 268,187 |

| Purchase | – Cash 14,440 – Credit 496,600 |

- Total receipts from customers 600,570

- Total payment to suppliers 503,970

- Discount allowed to credit customer 5,520

- Discount received from credit suppliers 3,510

- Refund given to cash customers 5,070

- Balance in sales ledger setoff against balance in the purchase ledger 700

- Bad debt written off 780

- Increase in the allowance for doubtful debts 900

- Credit note issued to credit customers 4,140

- Credit note received from credit suppliers 1,480

According to the audited financial statement for the previous year account receivable and account payable as to 1st December 2013 were 26,550 and 43,450 respectively

- Required;

Draw up the relevant total accounts entering end of year total for account receivable and account payable.

FORM THREE BKEEPING EXAM SERIES 192

FORM THREE BKEEPING EXAM SERIES 192

PRESIDENT OFFICE REGIONAL ADMINISTRATION

AND LOCAL GOVERNMENT

SECONDARY EXAMINATION SERIES

COMPETENCE BASED ASSESSMENT

FORM THREE

MID TERM EXAMS-AUG– 2023

062 BOOK KEEPING

Time: 2:30 Hours August, 2023

Instructions

- This paper consists of sections A, B and C with a total of nine (9) questions.

- Answer all the questions.

- Sections A carries fifteen (15) marks and B carries forty (40) marks and Section C carries forty-five (45) marks.

- All writings must be in blue or black ink.

- Non – programmable calculators may be used.

- All communication devices, programmable calculators and any unauthorized materials are not allowed in the examination room.

- Write your Examination Number on every page of your answer booklet (s).

SECTION A (15 Marks)

Answer all questions in this section

- For each of the items (i) – (x), choose the correct answer from among the given alternatives and write its letter besides the item number in the answer booklet provided:

- How could purchases of a non- current assets by cheques affect the statement of financial position?

- By decreasing non-current assets account and decreasing bank account

- By increasing bank account and decreasing asset account

- By increasing non-current asset account and decreasing cash account

- By increasing cash account and decreasing asset account

- By increasing non-current asset account and decreasing bank account

- Amount of surplus in a statement of income and expenditure account indicates:

- Excess of income over expenditure

- Excess of cash received over credit sales

- Excess of expenditure over income

- Excess of gross profit over expenses

- Excess of expenses over net profit

- Government expenditures on items from which the government attains no value are called.

- Development expenditure.

- Recurrent expenditure.

- Capital expenditure.

- Revenue expenditure

- Nugatory expenditure.

- Which items would appear under non-current liabilities in the statement of financial position?

- TZS 700,000/= 5 years Loan from NBC.

- TZS 900,000/= of Credit purchases

- TZS 500,000/= paid for expenses

- TZS 600,000/= 10 months Loan from NMB

- TZS 800,000/= 6 months Loan from CRDB

- On 20th July, 2023, Mtumzima, a sole trader purchased a machinery for cash paying TZS 3,500,000/=. What would be a double entry for this transaction?

- Debit: Cash account, Credit: Machinery account

- Debit: Purchases account, Credit: Machinery

- Debit: Machinery account, Credit: Purchases account

- Debit: Machinery Account, Credit: Bank account

- Debit: Machinery account, Credit: Cash account

- At the beginning of Accounting year, Wini Charity Foundation had TZS 140,000/= as non-current Assets, TZS 50,000/= as current Assets and TZS 60,000/= as liabilities. What would be its opening Accumulated fund?

- TZS 190,000/=

- TZS 200,000/=

- TZS 110,000/=

- TZS 130,000/=

- TZS 250,000/=

- Which of the following best describes Non-current assets?

- Expensive items bought for the business

- Items having long life and not bought for resale

- Items which will not wear out quickly

- Items which do not add value to a business

- Items bought to be used by the business

- ______________ are the books under which the transactions are entered before being posted to their respective ledgers.

- Accounts

- Subsidiary books

- Cash books

- Ledger books

- Note books

- “A company does not include the value of skills gained by its employees from training programs in its financial records.” Which accounting concept is applied?

- Dual aspect concept

- Matching concept

- Dual Aspect concept

- Money measurement concept

- Business entity concept

- A firm bought a Motor van for TZS 5,000,000 which had a scrap value of TZS 500,000, and useful life of 5 years. What would be the depreciation charge if a straight line method is used?

- TZS 1,000,000

- TZS 1,100,000

- TZS 900,000

- TZS 100,000

- TZS 500,000

- Match the items in Column A with the responses in Column B by writing the letter of the correct responses below the corresponding item number in the table provided.

| Column A | Column B |

|

|

SECTION B (40 Marks)

Answer all questions in this section.

- Complete the following table by identifying the account to be credited and debited as well:

| S/N | Transactions | Account to be debited | Account to be credited |

| i | Cash paid to Rahima |

|

|

| ii | A payment of rent by cash |

|

|

| iii | Sales of goods to Mtumzima |

|

|

| iv | Cash received from Julius |

|

|

| v | Purchased goods for cash |

|

|

- Use the knowledge of accounting equation to fill in the gap in the following table

| S/N | ASSETS | CAPITAL | LIABILITIES |

| i | TZS 3,500,000 | TZS 1,700,000 | TZS __________ |

| ii | TZS ___________ | TZS 8,000,000 | TZS 4,100,000 |

| iii | TZS 4,900,000 | TZS _________ | TZS 2,100,500 |

| iv | TZS 25,600,000 | TZS 17,900,000 | TZS __________ |

| v | TZS ____________ | TZS 15,500,000 | TZS 3,400,000 |

- Briefly describe the meaning of the following terms as used in book keeping:

- Accrued expenses

- Book keeping

- Credit transaction

- Carriage outwards

- Trial balance

- Winfrida is a business woman who owns a Jewels shop in Arusha. She is also a customer of CRDB bank. Winfrida prefers to settle her debts using cheques. In the last month, she wrote a cheque to Onesmo, her creditor, for which the bank refused to settle it. In five points outline the reasons for this to happen.

SECTION C (45 Marks)

Answer all questions in this section.

- Mtumzima Transport Company with the financial year ending on 31st December, bought two motor vans on 1st January 2011, No 1 for TZS 18,000,000 and No 2 for TZS 15,000,000. It also buys another van, No. 3 on 1st July 2012, for TZS 19,000,000 and another No 4 on 1st October, 2013 for TZS 17,200,000 the van No 1 was sold for TZS 6,290,000 on 30th September 2014. It is a company’s policy to charge depreciation at 15% per annum using a straight line method for each month of ownership basis.

Required: Prepare for the year ended 31st December, 2011, 2012, 2013 and 2014.

- Motor van account

- Accumulated Provision for depreciation account

- Motor van disposal account

- The following information is available from the books for Ethan Wholesale Store on 1st September, 2021:

Balances in purchases ledger TZS 120,000 (CR)

Balances in sales ledger TZS 7,100 (CR)

Balances in purchases ledger TZS 4,800 (DR)

Balances in sales ledger TZS 163,100 (DR)

During September 2021:

Sales 140,000

Purchases 88,000

Returns inwards from debtors 55,000

Returns outwards from creditors 7,300

Receipts from debtors 91,300

Payments to creditors 76,700

Discount allowed 4,000

Discount received 2,200

Bad debts written off 3,800

Debtors cheque dishonored 7,500

Interest charged to debtors on overdue accounts 500

Sales ledger debit transferred to purchases Ledger 9,600

Notes:

- 10% sales and discount allowed relate cash transactions

- 5% of the goods bought during the month were destroyed by fire, the insurance company had agreed to pay adequate claim.

You are required to prepare:

- A sales ledger control account

- A purchases ledger control account

- Mtumzima Entreprises had the following assets and liabilities on the date shown:

01.01.2021 31.12.2021

Premises 14,500 14,500

Motor cars 2,800 1,800 Furniture 3,500 3,200

Stock in Trade 11,200 13,100

Trade debtors 10,900 11,400

Trade creditors 14,600 17,200

Cash at bank 1,330 3,980

Prepaid expenses 670 1,120

Accrued expenses 1,300 600

During 2021, Mtumzima withdrew TZS 3,000 per month from the business bank account for his personal use. On 4 July 2021 he sold his personal car for TZS 12,000 and paid the proceeds into the business bank account.

Required:

Calculate the net profit or loss made by Mtumzima for year ended 31st December, 2021.

FORM THREE BKEEPING EXAM SERIES 149

FORM THREE BKEEPING EXAM SERIES 149

THE UNITED REPUBLIC OF TANZANIA PRESIDENT’S OFFICE

REGIONAL ADMINISTRATION AND LOCAL GOVERNMENT

FORM TREE MID TERM TEST MARCH-2023

033/1 BOOK-KEEPING

Time: 3 Hours MARCH, 2023

Instructions

- This paper consists of three sections A, B and C with a total of 9 questions.

- Answer all questions in section A and B and only two (2) questions from section C.

- Section A carries twenty (20) marks, section B forty (40) marks and section C forty (40) marks.

- Non programmable calculators may be used.

- Cellular phones, and other authorized materials are not allowed in the examination room.

- Write your examination number on every page of your Answer booklet(s).

SECTION A (20 MARKS)

Answer all questions in this section

1. for each of the items (i)-(xv), choose the correct answer from among the given

Alternatives and write its letter beside the item number in the answer sheet provided

- If sales is 20,000 and profit make up is 25%, determine the amount of cost price

- 13,600

- 12,000

- 16,000

- 12,900

- 20,600

- Which book of prime entry records the sale or purchase of non-current Assets?

- General journal

- Sales journal

- Purchases journal

- Cash book

- Sales return day book

- If cash sale amount to Tshs 100,000/= paid direct into the bank account, the correct double entry will be to

- Debit sales account and credit cash account by sh.100, 000

- Debit cash account and credit bank account by sh.100, 000

- Debit bank account and credit sales account by sh.100, 000

- Debit bank account and credit cash account by sh.100, 000

- Debit sales account and credit bank account by sh.100, 000

- How much is to be reimbursed if a petty cashier has spent Tsh.189,00/=while his cash float is Tsh.200,000/=

- Tsh,11,000/=

- Tsh 389,000/=

- Tsh,189,000/=

- Tsh,200,000/=

- Tsh,21,000/=

- Working capital is a term meaning.

- The excess of current liabilities over current liabilities

- The excess of the current assets over the current liabilities

- the excess of the current assets over non-current liabilities

- The excess of current assets over non-current assets.

- The excess of non-current Assets over current liabilities

- Natasha and Ndengwe share profits and losses in the ratio 3:2. Their partnership recorded net profits of shs. 1,400, interest on capital shs. 420, partners’ salaries shs. 100 and drawings shs. 280, Determine Ndengwe’s share of the profits.

- TZS 840

- TZS 560

- TZS 464

- TZS 696

- TZS 506

- From the following categories of errors, identify the category of errors which affect only one account

- Casting errors

- Errors of principle

- Errors of omission.

- Errors of original entry.

- Errors of commission.

- In the business of C. Sangster, who owns a clothing store, which of the following is the capital expenditure?

- Fixtures and New Van bought

- Shop fixtures bought and wages of assistants

- Wages of assistants and new van bought

- Wages of assistants and Petrol for Van

- Fixtures and salaries.

- Manufacturing account is used to calculate:

- Production cost paid in the year

- Total cost of goods produced

- Production cost of goods completed

- Gross profit on goods sold

- Prime cost of goods manufactured

- Depreciation can be described as the : _______

- Amount spent to buy a non –current asset

- Salvage value of a non-current asset consumed during its period

- Cost of the non-current asset consumed during its period

- Amount of money spent replacing non-current asset

- Cost of old asset plus new assets purchased

- A bank reconciliation statement is a statement:

- Sent by bank when the account are overdrawn

- Drawn to verify cash book balance with the bank statement balance

- Drawn up by the bank to verify the cash book

- Sent by the bank to the customers when errors are made

- Sent by the bank customers to the friends.

- If two totals of trial balance do not agree, the difference must be entered in:

- A real account

- The trading accounts

- A nominal account

- The capital account

- A suspense account

- The accounting equation is expressed in the financial statement called:

- statement of financial position

- income statement

- expenditure statement

- reconciliation statement

- statement of change in equity

- If we take goods for own use, we should

- Debit drawings Account: Credit Purchase Account

- Debit Purchases Account: Credit Drawings Account

- Debit Drawings Account: Credit Inventory Account

- Debit Sales Account: Credit Inventory account

- debit inventory Account: Credit Drawing Account

- if a partnership maintains a fixed capital account, then the partner’s share

of profits is:

- Credited to the partner’s drawings account

- debited to the partner’s capital account

- credited to the partner’s capital account

- credited to the partner’s current account

- debited to the partner’s current account

2. For each of the items (i)-( v) match the narrations of bank reconciliation Items in column A with their corresponding names in column B by writing the letter of the correct response beside the item number in the answer sheet provided

| COLUMN A | COLUMN B |

|

|

SECTION B (40 MARKS)

Answer all questions in this section.

3. In 1991 Mr. Chipepeto bought a motor car for the cost value of sh.8, 000,000/= with the aim of assisting him in business. But three years later he decided to dispose it for a book value of sh.6,700,000/=

- What is the term used to mean the difference between cost value and book value.

- Outline four reasons that could be the causes for him to dispose the car for less than the cost value.

4. The DSM Rotary club, has provided you with the following information:-

| As at 31st December | 2000 | 2001 |

| Subscription in arrears | 6400 | 8800 |

| Subscription in advance | 1200 | 3400 |

| Subscription during the year | - | 20,200 |

| Insurance expenses owing (in arrears) | 3700 | 2700 |

| Insurance expenses prepaid (in advance) | 4400 | 5200 |

| Insurance paid during the year | - | 16,800 |

Required: Prepare A Subscription account and Insurance account, clearly showing amounts to be transferred to income and expenditure accounts for year 2001.

5. Define the following terms

- Discount received

- Invoice

- Discount allowed

- Carriage inwards

- Carriage outwards

6. (a) Mr. Kyamba wants to start a business, but before commencement he needs to learn book keeping. Outline five objectives for him to study book keeping.

(b) Briefly explain three types of a cash book.

SECTION C (40 MARKS)

Answer two questions only from this section.

7. Panguso& company limited own a manufacturing industry which had the following records for the year ended at 31st December 2007.

- Inventory at 1st January 2007:

- raw materials sh.760, 000

- Finished goods sh 360,000

- Purchases of raw material sh.420, 000

- Sales of finished goods sh.2, 490,000

- Factory Fuel & power sh.320, 000

- Royalty sh.500, 000

- Depreciation of works machine sh.88, 000

- Market value sh.1,800,670

- General office expense sh.10, 740

- Manufacturing wages sh.170, 000

- Inventory at 31 stDec 2007: raw material sh.900, 000

- Finished goods sh.580, 000

- Works in progress sh.734, 000

You are required to prepare

- Statement of manufacturing costs for the year ended at 31 stDec 2007

- Income statement for the year ended at 31.12.2007

8. XY Ltd provides for depreciation of its machinery at 20% per annum on cost; it charges for a full year in the year of purchase but no provision is made in year of sale/disposal.

Financial statements are prepared annually to 31th December. 2015

- January 1 Bought machine ‘A’ 10,000

- July 1 Bought machine ‘B’ 6,000

2016

- March 31 Bought machine ‘B’ 8,000

2017

- October 7 Sold machine ‘A’ – proceeds 5,500

- November 5 Bought machine ‘D’ 12,000

2018

- February 4 Sold machine ‘B’ – proceeds 3,000

- February 6 Bought machine ‘B’ 9,000

- October 11 Exchanged machine ‘D’ for machine valued at 7,000

Prepare;

- The machinery account for the period 1st January 2015 to 31st December 2018

- The accumulated provision for depreciation on machinery account, for the period 1st January 2015 to 31st December 2018.

9. The financial of the GGM trading company ended on 30th November 2014. You have been asked to prepare a total amount receivable and total amount payable for the draft final amounts. You are able to obtain the following information for the financial year the book of original entry.

| Sales | – Cash 344,890 – Credit 268,187 |

| Purchase | – Cash 14,440 – Credit 496,600 |

- Total receipts from customers 600,570

- Total payment to suppliers 503,970

- Discount allowed to credit customer 5,520

- Discount received from credit suppliers 3,510

- Refund given to cash customers 5,070

- Balance in sales ledger setoff against balance in the purchase ledger 700

- Bad debt written off 780

- Increase in the allowance for doubtful debts 900

- Credit note issued to credit customers 4,140

- Credit note received from credit suppliers 1,480

According to the audited financial statement for the previous year account receivable and account payable as to 1st December 2013 were 26,550 and 43,450 respectively

- Required;

Draw up the relevant total accounts entering end of year total for account receivable and account payable.

FORM THREE BKEEPING EXAM SERIES 122

FORM THREE BKEEPING EXAM SERIES 122

THE PRESIDENT’S OFFICE MINISTRY OF EDUCATION, REGIONAL ADMINISTRATION AND LOCAL GOVERNMENT

COMPETENCY BASED SECONDARY EXAMINATION SERIES

BOOK KEEPING FORM THREE

Time: 2:30 Hours November, 2022

Instructions

- This paper consists of sections A, B and C with a total ofnine (9) questions.

- Answer all questions in sections A and B and two (2) questions from section C.

- Section A carries twenty (20) marks, section B forty (40) marks and section C carries forty (40) marks.

- All writings should be in blue or black ink pen and all drawings should be in pencil.

- Non programmable calculators may be used.

- Cellular phones, programmable calculators and any unauthorized materials are not allowed in the examination room.

SECTION A (20 Marks)

Answer all questions in this section

- For each of the items (i) – (xv), choose the correct answer from among the given alternatives and write its letter besides the item number in the answer booklet provided:

- How could a purchases of a non- current assets by cheques affect the statement of financial postion?

- By decreasing non-current assets account and decreasing bank account

- By increasing bank account and decreasing asset account

- By increasing non-current asset account and decreasing cash account

- By increasing cash account and decreasing asset account

- By increasing non-current asset account and decreasing bank account

- Which of the following errors would be disclosed by the Trial Balance?

- Credit sales of TZS 20,000/= entered in the books as TZS 2,000/=

- Cheque for TZS 65,000/= from R.James entered in R.James as TZS 59,000/=

- Cash sales TZS 100,000 were completely omitted in the books

- Selling expenses TZS 5,000 had been debited to sales Account.

- A purchase of goods worth TZS 2,500/= omitted from the books

- Which of the following depreciation methods uses the reduced value to compute the depreciation of non-current assets?

- Straight line method

- Sum of the years’ digit methods

- Diminishing balance method

- Unit of output method

- Revaluation method

- At the beginning of Accounting year, a club had TZS 14,000/= as non-current Assets, TZS 5,000/= as current Assets and TZS 5,000/= as liabilities. What would be its opening Accumulated fund?

- TZS 4,000/=

- TZS 14,000/=

- TZS 12,000/=

- TZS 24,000/=

- TZS 10,000/=

- Form three students were arguing on which primary and basic objective of preparing a trial balance is. Which of the following uses is the basic purpose of preparing a trial balance?

- A trial balance is used for internal control as back up document

- A trial balance is used as a tool for preparing financial statements

- A trial balance is used to check arithmetical accuracy of double entry

- A trial balance is used to present a list of balances at one place

- A trial balance is used to determine profit or loss of a business

- Which of the following are the examples of revenue expenditure?

- Purchases of goods and payment for electricity bill in cash

- Repair of van and petrol costs for van

- Buying machinery and paying for installation costs

- Electricity costs of using machinery and buying van

- Wages paid to the worker who operates a machinery

- Money contributed by individuals under non-profit marking organization is known as:

- Capital introduced

- Capital owed

- Capital employed

- Working capital

- Accumulated fund

- A firm bought a machine for TZS 16,000/=. It is expected to be used for 5 years then sold for TZS 1,000/=. What is the annual amount of depreciation if the straight-line method is used?

- TZS 3,200/=

- TZS 3,100/=

- TZS 3,750/=

- TZS 3,000/=

- TZS 6,000/=

- When business entity paid rent of TZS 800,000/=. The payment was recorded in the books as follows. Debit: “Bank” TZS 800,000/= and Credit: Rent TZS 800,000/=. What entries will be posted to rectify this error?

- Debit “Bank” TZS 800,000/= and credit “Rent” TZS 800,000/=

- Credit “Rent” TZS 800,000/= and credit “Bank” TZS 800,00/=

- Debit “Bank” TZS 800,000/= and Credit “Rent” TZS 1,600,000/=

- Debit “Rent” TZS 1,600,000/= and credit “Bank” TZS 1,600,000/=

- Debit “Bank” TZS 1,600,000/= and credit “Rent” TZS 1,600,000/=

- Baraka wants to start up a business dealing with Clothing Wholesale Store, but he does not have enough capital to commence his business. The following can be used as the sources of capital for his business EXCEPT:

- Money borrowed from bank

- Money saved for business start up

- Money saved for building a private house

- Cash received from the sales of shares

- Cash received from the sale of his private car

- Government expenditures on items from which the government attains no value are called.

- Development expenditure.

- Recurrent expenditure.

- Capital expenditure.

- Revenue expenditure

- Nugatory expenditure.

- A business owned by Esther had an opening and closing capital balances of TZS 57,000/= and TZS 64,300/= respectively. The drawings during the same year amounted to TZS 11,800/=. What was the amount of profit made by her business during that year?

- TZS 19,100/=

- TZS 16,600/=

- TZS 5,000/=

- TZS 19,600/=

- TZS 18,600/=

- Mtumzima Art Creators is a registered company dealing with production and supply of the artistic works. During October 2022, it Purchased machinery for cash costing TZS 35,000,000/=. What will be a double entry for this transaction?

- Debit Cash account, Credit Machinery account

- Debit Purchases account, Credit Machinery

- Debit machinery account, Credit Cash account

- Debit Purchases account , Credit cash account

- Debit purchases account, Credit machinery account

- What is the effect of TZS 500,000/= being added to Purchases instead of being added to a non-current asset?

- Net profit would be understated

- Net profit would be overstated

- Both Gross profit and Net profit would be understated

- Net profit would not be affected

- Gross profit would be affected

- Depreciation can be described as the

- Amount spent to buy a non-current asset.

- Salvage value of a non-current asset.

- Cost of the non-current asset consumed during its period.

- Amount of money spent replacing non-current asset.

- Cost of old assets plus new purchased.

- If the Assets of the business amounted to TZS 85,000/= and Owner’s Capital is TZS 60,000/= How much is the Liabilities of the business?

- TZS. 45,000/=

- TZS. 145,000/=

- TZS.25,000/=

- TZS.85,000/=

- TZS 60,000/=

- For each of the items (i) – (v), match the descriptions of correction of errors terms in Column A with their corresponding names in Column B by writing the letter of the correct response beside the item number in the answer sheet:

| COLUMN A | COLUMN B |

| A. Error of complete reversal entries B. Error of compensating C. Error of commission D. Error of principle E. Error of original entry F. Error of omission G. Transposition error |

SECTION B (40 Marks)

Answer all questions in this section

- Briefly describe the meaning of the following terms as used in book keeping:

- Accrued expenses

- Book keeping

- Credit transaction

- Carriage outwards

- Net profit

- Upendo is a business woman who owns a Jewels shop in Arusha. She is also a customer of CRDB bank. Upendo prefers to settle her debts using cheques. In the last month, she wrote a cheque to Onesmo, her creditor, for which the bank refused to settle it. In five points outline the reasons for this to happen.

- On 31st December 2017, the cash book balance of ShedrackTraders was TZS 25,370/= where the bank statement showed a credit balance of TZS 25, 670/=. In comparing these two balances, the following were discovered;

- Cheques not yet presented for payment TZS 12,340/=

- Cheques paid into the bank but not yet credited by the bank account TZS 12,160/=

- Items shown in the bank statement but not yet entered in the cash book were as follows:

- Bank charges TZS 240/=

- Standing order TZS 460/=

- Dividends collected by the bank TZS 820/=

Required:

- Bring the cash book to date to show the correct cash book balance.

- Prepare a bank reconciliation statement starting with the adjusted cash book balance.

- Rule a petty cash book under the following headings: - Postage, stationery, Petrol, entertainment and ledger.

2020 TZS

March 12 Petty cashier received cash from main cashier…………………. 15,000

14. Paid postage………………………………………….. 500

16. Paid entertainment…………………………………… 3,000

18. Paid petrol…………………………………………….. 1,200

20. Paid B. Robert, a creditor……………………………… 4,000

25. Paid for stationery…………………………………… 1,700

29. The cashier reimbursed the petty cashier the amount spent in the period.

SECTION C (40 Marks)

Answer two (2) questions from this section.

- Mtumzima Transport Company with the financial year ending on 31st December, bought two motor vans on 1st January 2011, No 1 for TZS 18,000,000 and No 2 for TZS 15,000,000. It also buys another van, No. 3 on 1st July 2012, for TZS 19,000,000 and another No 4 on 1st October, 2013 for TZS 17,200,000 the van No 1 was sold for TZS 6,290,000 on 30th September 2014. It is a company’s policy to charge depreciation at 15% per annum using a straight line method for each month of ownership basis.

Required: Prepare for the year ended 31st December, 2011, 2012, 2013 and 2014.

- Motor van account

- Accumulated Provision for depreciation account

- Motor van disposal account

- The following trial balance has been extracted from the ledger of Julius, a sole trader.

Trial balance as at 31st May, 2022

| S/N | Name of account | DR | CR |

| 1 | Purchases and sales | 82,350 | 138,078 |

| 2 | Carriage | 5,144 | |

| 3 | Drawings | 7,800 | |

| 4 | Rent, rates and insurance | 6,622 | |

| 5 | Postage and stationery | 3,001 | |

| 6 | Advertising | 1,330 | |

| 7 | Salaries and wages | 26,420 | |

| 8 | Bad debts | 877 | |

| 9 | Allowance for doubtful debts | 130 | |

| 10 | Accounts receivables and payables | 12,120 | 6,471 |

| 11 | Cash in hand | 177 | |

| 12 | Cash at bank | 1,002 | |

| 13 | Inventory as at 1.6.2021 | 11,927 | |

| 14 | Equipment (at cost) | 58,000 | |

| 15 | Accumulated depreciation on equipment | 19,000 | |

| 16 | Capital | 53,091 |

The following additional information as at 31st May, 2022 is available:

- Rent is accrued by TZS 210/=

- Rates have been prepaid by TZS 880/=

- TZS 2,211 of carriage represent carriage on purchases

- Equipment is to be depreciated at 15% p.aon cost.

- The allowance for doubtful debts to be increased by TZS 40/=

- Inventory at the close of business has been valued at TZS 13,551/=

Required:

Prepare Julius’s Income statement for the year ending 31st May, 2022 and a Statement of financial position as at that date.

- The following information is available from the books for Abigail Wholesale Store on 1st September, 2021:

Balances in purchases ledger TZS 120,000 (CR)

Balances in sales ledger TZS 7,100 (CR)

Balances in purchases ledger TZS 4,800 (DR)

Balances in sales ledger TZS 163,100 (DR)

During September 2021:

Sales 140,000

Purchases 88,000

Returns inwards from debtors 55,000

Returns outwards from creditors 7,300

Receipts from debtors 91,300

Payments to creditors 76,700

Discount allowed 4,000

Discount received 2,200

Bad debts written off 3,800

Provision for bad debts increased by 600

Debtorscheque dishonored 7,500

Interest charged to debtors on overdue accounts 500

Sales ledger debit transferred to purchases Ledger 9,600

Notes:

- 10% sales and discount allowed relate cash transactions

- 5% of the goods bought during the month were destroyed by fire, the insurance company had agreed to pay adequate claim.

You are required to prepare:

- A sales ledger control account

- A purchases ledger control account

FORM THREE BKEEPING EXAM SERIES 106

FORM THREE BKEEPING EXAM SERIES 106

THE PRESIDENT’S OFFICE MINISTRY OF EDUCATION, REGIONAL ADMINISTRATION AND LOCAL GOVERNMENT

COMPETENCY BASED SECONDARY EXAMINATION SERIES

FORM THREE EXAMINATION

062 BOOK-KEEPING

![]() Time: 2:30 Hours Sept, 2022

Time: 2:30 Hours Sept, 2022

Instructions

- This paper consists of sections A, B and C with a total of nine (9) questions.

- Answer all questions in sections A and B and two (2) questions from section C.

- Section A carries twenty (20) marks, section B forty (40) marks and section C carries forty (40) marks.

- All writings should be in blue or black ink pen and all drawings should be in pencil.

- Non programmable calculators may be used.

- Cellular phones, programmable calculators and any unauthorized materials are not allowed in the examination room.

SECTION A (20 Marks)

Answer all questions in this section

- For each of the items (i) – (xv), choose the correct answer from among the given alternatives and write its letter besides the item number in the answer booklet provided:

- Mtumzima bought 5 items of TZS 800 each, and given allowance of 25% trade discount and 5% cash discount, if he could settle within the agreed credit period, how much was paid?

- TZS 2,850

- TZS 2,800

- TZS 2,600

- TZS 4,000

- TZS 3,000

- Mr. MRAMBA as a Petty cashier was given a desired cash float of TZS 100,000/= if TZS 72,000/= is spent by him, under imprest system of petty cash how much will be reimbursed?

- TZS 28,000/=

- TZS 172,000/=

- TZS 72,000/=

- TZS 70,000

- TZS 100,000/=

- The book value of an Asset after two years, using straight line method at 10% was TZS 10,000/=. What was the cost price of the Asset?

- TZS 20,000/=

- TZS15,000/=

- TZS 12,500/=

- TZS 10,000/=

- TZS 30,000/=

- Amount of surplus in a statement of income and expenditure account indicates:

- Excess of income over expenditure

- Excess of cash received over credit sales

- Excess of expenditure over income

- Excess of gross profit over expenses

- Excess of expenses over net profit

- Which of the following errors would be disclosed by the Trial Balance?

- Credit sales of TZS 20,000/= entered in the books as TZS 2,000/=

- Cheque for TZS 65,000/= from R.James entered in R.James as TZS 59,000/=

- Cash sales TZS 100,000 were completely omitted in the books

- Selling expenses TZS 5,000 had been debited to sales Account.

- A purchase of goods worth TZS 2,500/= omitted from the books

- Government expenditures on items from which the government attains no value are called.

- Development expenditure.

- Recurrent expenditure.

- Capital expenditure.

- Revenue expenditure

- Nugatory expenditure.

- What is the effect of TZS 500,000/= being added to Purchases instead of being added to a non-current asset?

- Net profit would be understated

- Net profit would be overstated

- Both Gross profit and Net profit would be understated

- Net profit would not be affected

- Gross profit would be affected

- At the beginning of Accounting year, a club had TZS 14,000/= as non-current Assets, TZS 5,000/= as current Assets and TZS 5,000/= as liabilities. What would be its opening Accumulated fund?

- TZS 4,000/=

- TZS 14,000/=

- TZS 12,000/=

- TZS 24,000/=

- TZS 10,000/=

- When the financial statements are prepared, the bad debts Account is closed by being transferred to: -

- Statement of financial position

- Provision for doubtful debts Account

- Income statement

- Statement of affairs

- Trading account

- When business entity paid rent of TZS 800,000/=. The payment was recorded in the books as follows. Debit: “Bank” TZS 800,000/= and Credit: Rent TZS 800,000/=. What entries will be posted to rectify this error?

- Debit “Bank” TZS 800,000/= and credit “Rent” TZS 800,000/=

- Credit “Rent” TZS 800,000/= and credit “Bank” TZS 800,00/=

- Debit “Bank” TZS 800,000/= and Credit “Rent” TZS 1,600,000/=

- Debit “Rent” TZS 1,600,000/= and credit “Bank” TZS 1,600,000/=

- Debit “Bank” TZS 1,600,000/= and credit “Rent” TZS 1,600,000/=

- A business had an opening and closing capital balances of TZS 57,000/= and TZS 64,300/= respectively. The drawings during the same year amounted to TZS 11,800/= What was the amount of profit made by the business during that year?

- TZS 19,100/=

- TZS 16,600/=

- TZS 5,000/=

- TZS 19,600/=

- TZS 18,600/=

- Gloria General store sold goods worth TZS 100,000/= to Joshua on credit and were neither recorded in sales account nor in Pearl’s personal account. This represents an error of:

- Error of commission.

- Error of omission.

- Error of original entry

- Error of principle.

- Error of complete reversal of entries.

- Jeff and Witness were arguing on the primary and basic reason of preparing a trial balance. As form three student taking business studies, what is the basic reason for writing up a trial balance among the following reasons?

- A trial balance issued for internal control as back up document.

- A trial balance is used as a tool for preparing financial statement.

- A trial balance is used to determine a reliable financial position

- A trial balance is used to present a list of balances at one place.

- A trial balance is used to check arithmetical accuracy of double entry.

- Which of the following are the examples of revenue expenditure?

- Purchases of goods and payment for electricity bill in cash

- Repair of van and petrol costs for van

- Buying machinery and paying for installation costs

- Electricity costs of using machinery and buying van

- Purchases of office equipment

- A firm bought a Motor van for TZS 50,000 which had a scrap value of TZS 5,000, and useful life of 5 years. What would be the depreciation charge if a straight line method is used?

- TZS 10,000

- TZS 11,000

- TZS 9,000

- TZS 1,000

- TZS 5,000

- Match the items in Column A with the responses in Column B by writing the letter of the correct responses below the corresponding item number in the table provided.

| Column A | Column B |

|

|

SECTION B (40 Marks)

Answer all questions in this section.

- Book keeping involves the recording on a daily basis of a company’s financial transactions whether on single entry system or double entry system and because of book keeping, companies are able to track all financial information on its books to make key operating, investing, and financing decisions. Outline five reasons stating why double entry system is better in book keeping.

- On 1st July, 2017 Mtumzima Company bought a machinery for TZS 18,000,000, and decided to sell it for TZS 12,000,000 after using it for four (04) years. In four (04) points describe briefly why the company decided to sell a machinery at a price lower than the original cost price.

- Prepaid rent at the beginning of the period was TZS 40,000/= and TZS 20,000/= was not paid last year. During the year payment of TZS 320,000/= was made with respect to rent. It was established that at the end of the period prepaid rent should be TZS 60,000/=. Compute the amount of Rent Expenses to be transferred to income statement.

- The following information relates with Star social club for the year ended 31st June 2020.

![]() 1.7.2019 31.6.2020

1.7.2019 31.6.2020

Subscription in arrears 4,500 3,200

Subscription received in advance 6,300 1,800

During the year, the subscriptions amounted to TZS. 120,000 were received from the club members.

Required:

Subscription account, showing the amount to be transferred to the statement of Income and expenditures for year ended 31st June, 2020.

SECTION C (40 Marks)

Answer two (2) questions from this section.

- SIJAFELI keeps his books on a single entries system. The following are the balances of Assets and Liabilities of his business for the year ended 31st December, 2017.

Receipts and Payments made for cash during the year were as follows:

Receipts from Debtors ______________________________________420,000

Payment to Creditors ______________________________________200,000

Carriage inwards ___________________________________________ 40,000

Drawings _________________________________________________120,000

Sundry Expenses __________________________________________140,000

Purchases of new furniture ___________________________________ 20,000

Other information:

There was a considerable amount of cash sales. Depreciate furniture at 10% on a closing balance.

From the information provided, prepare

- Accounts receivables and Accounts payables control Accounts

- Cash Account.

- Income statement for the year ended 31st December 2017

- Statement of financial position as at 31st December 2017

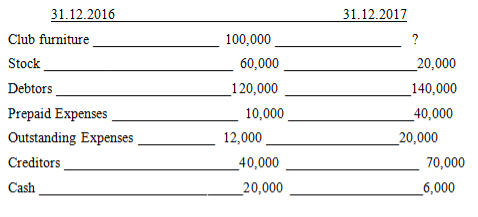

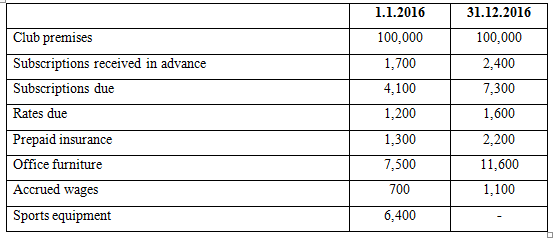

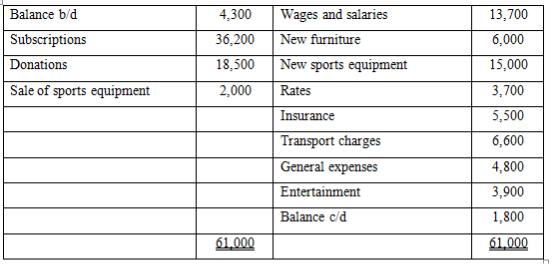

- MtumzimaSports Club, a non-profit making organization was looking for a form three student who is able to assist them in the preparations of various accounts and statements for payments. In their interview one of the questions was as follows: -

Assets and Liabilities:

Receipts and Payments Account

The following information were also available

- The sports equipment sold during the year had a book value of sh.3,500/=

- Depreciation on sports equipment was provided at 20% per year

Required:

- A statement of affairs as at 1.1.2016

- Subscription account

- A statement of Income and expenditure for the year ended at 31.12.2016

- A statement of financial position as at that date.

- The financial year of Collins Trading Company ended on 31.12.2017. You have been asked to prepare a Total Debtors Account and a Total Creditors Account in order to produce end-of-year figures for Debtors and Creditors for the draft financial statements.

You are able to obtain the following information for the financial year from the books oforiginal entry:

TZS

Sales made on Cash basis 782,500

Sales made on Credit 368,187

Purchases made on Cash basis 214,440

Purchases made on Credit 596,600

Total cash receipts from customers 300,570

Total cash payments to suppliers 503,970

Discounts allowed (all to credit customers) 5,520

Discounts received (all from credit suppliers) 3,510

Refunds given to cash customers 5,070

Balance in the sales ledger set off

against balance in the purchases ledger 700

Bad debts written off 780

Credit notes issued to credit customers 4,140

Credit notes received from credit suppliers 1,480

According to the audited financial statements for the previous year debtors and creditors as at 1.1.2017 were TZS 26,555 and TZS 43,450 respectively.

Required:

- Accounts receivables Control Account

- Accounts payables Control Account

Page 1 of 10

FORM THREE BKEEPING EXAM SERIES 98

FORM THREE BKEEPING EXAM SERIES 98

THE PRESIDENT’S OFFICE MINISTRY OF EDUCATION, LOCAL ADMINISTRATION AND LOCAL GOVERNMENT

BOOKEEPING- TERMINAL EXAMINATION-MAY

FORM THREE

TIME: 2½HRS 2020

NAME:______________________________CLASS:___________

INSTRUCTIONS

- Answer all questions

1. Choose the correct answer from the given alternatives write its letter beside the item number

(i) Which of the following is a liability?

- Debtor

- Loan from exim bank

- Building

- Prepaid expenses

(ii) The cash payment of T.shs 439,000 to Juma would appear as follows:

- Credit Juma account, credit cash account

- Debit Juma account, credit cash account

- Debit bank account, credit Juma account

- Debit cash account, credit Juma account

(iii) Which of the following are personal accounts?

- Building and machine

- Wages and salaries

- Account receivable and account payables

- Profits and loss

(iv)In the trial balance, accumulated provision for depreciation account is

- Shown as a credit item

- Not shown as it is part of depreciation

- Shown as a debit item

- Sometimes shown as a credit, sometimes as a debit

(v) Which of the following is not correct?

- Assets – capital=liabilities

- Liabilities + capital=assets

- Liabilities + Assets=capital

- Assets – liabilities =capital

(vi) Which of the following should be charged in the trading, profit and loss account(income statement)

- Office rent

- Work-in-progress

- Direct materials

- Carriage on raw materials

(vii) At the end of trading period, bad debt account is closed and transferred to the

- Balance sheet

- Profit and loss account

- Trading account

- Allowance for doubtful debits account

(viii) Revenue expenditure is

- The extra capital paid in buying non-current assets

- The extra purchase of goods for sale

- Money spent on selling fixed assets

- The cost inairred in running the business on a day to day basis

(ix) An allowance made on the date of sales in respect of the date of payment is

- Discount allowed

- Cash discount

- Trade discount

- Quantity discount

(x) If shs 1000/= was added to purchases instead of being added to a fixed asset

- Net profit only would be understated

- Net profit only would be overstated

- Both gross profit and net profit would be understated

- Both gross profit and net profit would be overstated

2. Match the following by choose the correct answer from column B and write its letter beside the item number in column A

| Column A | Column B |

| (i) An item is entered in the wrong class of account (ii) Where errors cancel each other (iii) Where transaction is completely omitted from the books (iv) Where correct accounts are used but each item is shown on the wrong side of an account (v) Where correct amount is entered in the wrong account (vi) Where incorrect amount is entered in the accounts (vii) Incorrectly adding up figures to give an answer which is less than it should be (viii) Used to set the amount which will make the trial balance to balance when is affected by errors (ix) When transaction is posted twice in along the correct principles of double entry system (x) Errors committed when dualistion aspect of a transaction is not followed |

|

SECTION B

3. Write short notes on the following

- Capital expenditure

- Bad debts

- Depreciation of non-current asset

- Manufacturing account

- Single entry system

4. Kibaha education centre had received house rent for 1982 amounting to sh. 72,000. Out of this amount shs. 4,000 related to the year ending December 1983.

Required:

Rent received account to show the amount transferred to the profit and loss account

SECTION C

5. Jangua started business on 1st January 1993. Purchases and disposals of machines over three years were as follows.

| machine | Date of purchase | Cost(shs) | Date of disposal | Disposal proceeds(shs) |

| MAI | 1Jan 1993 | 5000,000 | - | - |

| MB 2 | 1Jan 1993 | 2500,000 | 1 Jan 1995 | 900,000 |

| MC 3 | 1 Jan 1995 | 7000,000 | - | - |

The machines are depreciated on straight line method using rate of 20% per annum

Required:

- Machine account

- Provision for depreciation account

- Disposal of machines account

6. K owns a store, her records are incomplete. You have been called in to prepare her accounts.

Through investigation the following information was obtained

01.01.2013 31.12.2013

Stock 2,100 2,240

Trade creditors 960 1,000

Motor vans 1,200 1,000

Debtors 1,300 1,040

Rates pre-paid 80 96

Cash at bank 900 2,344

Additional information

Drawings during the year amounted to Tshs 120 per week

Legacy of Tsh.400 received on March 2013 had been paid into the business bank account

Required