PRIME MINISTER’S OFFICE REGIONAL ADMINISTRATION AND LOCAL GOVERNMENT

FORM FOUR SECONDARY TERMINAL EXAMINATION

062 BOOK KEEPING

(For both school and private candidates)

Time: 3: 00 Hours

Instructions

- This paper consists of sections A, B and C with a total of nine (9) questions.

- Answer all questions.

- Section A carries fifteen (15) marks, section B forty (40) marks and section C carries forty-five (45) marks.

- All writing must be in blue or black ink.

- Non – programmable calculators may be used.

- Cellular phones and any unauthorized materials are not allowed in the examination room.

- Write your examination number on every page of your answer booklet(s) or sheet(s) provided.

SECTION A: (15 Marks)

Answer all questions

1. For each of the items (i) - (x) choose the correct answer from among the given alternative and write its letter beside the item number in the answer booklet provided

i. Tshs 500 cash taken from the cash till and banked is entered

- Debit cash column Tshs. 500: Credit bank column Tshs. 500

- Debit bank column Tshs. 500: Credit cash column Tshs. 500

- Debit bank column Tshs. 500: Credit bank column Tshs. 500

- Debit cash column Tshs. 500: Credit cash column Tshs. 500

- Debit bank column Tshs. 500

ii. The capital in the business at start of the year was Tshs. 120,000. At the end of the year was Tshs. 142,000. Drawing was Tshs. 1,000 per month. What was the net profit for the year?

- Tshs. 21,000

- TShs. 35,000

- TShs. 22,000

- TShs. 34,000

- TShs. 23,000

iii. If a non-trading organization operates a bar for profit purpose which of the following would determine if that activity made a profit or loss

- Receipts and payments account

- Subscription account

- Income statement

- receipts and expenditure statement

- Statement of financial position

iv. A business has the cost of goods sold worth TShs.150,000 and the mark-up of 40%. Calculate the amount of sales for the business

- TShs. 210,000

- TShs. 90,000

- TShs. 102,000

- Tshs. 150,000

- TShs 60,000

v. When comparing the performance of individual departments, which of the following statement should be compiled?

- Department account

- Statement of financial position

- Departmental current account

- Departmental income statement

- departmental income and expenditure

vi. Kulwa and Dotto share profits and losses in the ratio 3:2. Their partnership recorded net profit of Tshs 1,400, interest on capital Tshs 420, partner’s salaries Tshs 100 and drawings TShs 280. Determine Dotto's share of the profit

- 840

- 650

- 506

- 464

- 560

vii. When customer return goods previous sold to him, the shopkeeper will use a document called

- Credit note

- Order note

- Invoice

- Debit note

- Purchases order

viii. The following are the source of documents

- Cheque, invoice, cheque paid

- Invoice, cash receipts, debit note

- Sales, credit note, cheque

- Credit note, debit note, cash

- purchases, cash, cheque paid

ix. Which of the following is not correct about the petty cashbook?

- It reduce the number of entries in the nominal ledger

- The cash spent every month is fixed

- Cash spent is reimbursed every end of period

- Petty cashier receives cash from chief cashier

- Cash spent is reimbursed at the end of the year

x. In government accounting a term family is referred to

- Mother, wife and children

- All relatives

- Wife and children

- Father, wife and children

- Mother, father, wife and children

2. For each of the items (i) – (v), match the descriptions of the items in Column A with their corresponding names in Column B by writing the letter of the correct response beside the item number in the answer sheets provided:

| COLUMN A | COLUMN B |

| i. The expenses that the business has incurred but not yet paid for at the end of accounting period. ii. The amount of revenue that business expects to receive but has not yet been received at the end of accounting period. iii. The expenses which have been paid in advance, the benefits from which will be received in the next period. iv. The amount of revenue which has already been received in the current accounting but related to the following financial year. v. The cumulative sum of all depreciation expenses recorded for an asset. |

|

SECTION B: (40 Marks)

Answer all questions from this section

3. Mashaka who owned a retailer business, is not aware of accounting concepts and principles, explain to him the following concepts so that he can understand and apply in his business

- Money measurement concept

- Business entity concept

- Historical cost concept

- Dual aspect concept

- Going concern concept

4. Maige company Traders failed to prepare correct trial balance as seen below. You as a student who is expected to sit for National Examination this year 2024. Assist Maige Co. Traders to prepare correct trial balance basing to accounting principles and concepts.

| S/N | PARTICULARS | FOLIO | DEBIT | CREDIT |

| 1 | Wages | 2,500 | ||

| 2 | Stock | 3,500 | ||

| 3 | Creditors | 10,000 | ||

| 4 | Capital | 26,000 | ||

| 5 | Water bills | 15,000 | ||

| 6 | Discount allowed | 4,000 | ||

| 7 | Interest received | 6,000 | ||

| 8 | General expenses | 1,000 | ||

| 9 | Discount received | 7,200 | ||

| 10 | Insurance | 8,000 | ||

| 11 | Machine | 9,500 | ||

| 12 | Land | 7,800 | ||

| 13 | Debtors | 2,300 | ||

| 14 | Maintenance of machines | 6,500 | ||

| 15 | Advertising | 1,800 | ||

| 16 | Sales | 5,000 | ||

| 17 | Purchases | 7,000 | ||

| 18 | Loan from said | 36,600 | ||

| 19 | Cash at Bank | 21,900 | ||

| 90,800 | 90,800 |

5. The following transactions were obtained from the books Mchonga Motor cycle spare parts for the month of September 2016.

- 2nd Sold the following to Zuberi on credit 20 tyres @ TShs 30,000 and 6 boxes of oil @ TShs 10,000, less 20% discount

- 8th Sold on credit to Mussa 16 boxes of bulbs @ TShs 10,000 and 10 side mirrors @ TShs 12,000 less 15% discount

- 19th Credit to A. MpiliTShs 24,000

- 25th Sold on credit to Mazengo 7 used motorcycles @ TShs 100,000 and 14 boxes of rubber @ TShs 15,000 less 25% discount

- 28th sold on credit spare parts to Josky TShs 30,000

Required

Enter the above transactions in the sales Journal

6. You are well experienced and good book keeper, identify five (5) challenges facing the government accounting system in Tanzania.

SECTION C (40 Marks)

7. From the following transaction prepare the suspense Account and pass the Journal entries to rectify the following errors. Assuming that at the end of the trading period it was discovered that there was a difference of TShs 35,670 which was debited to the suspense account

- TShs 17,500 paid in cash for new electronic typewriter had been charged to office expenses account.

- Drawing amounting worth TShs 12,500 by cheque were completely omitted from the books.

- A purchase of goods from M. Batanga for TShs 25,000 were credited to the account of M. Batanga.

- Sales of goods worth TShs 9,600 made to Meshack Co. Ltd account was correctly entered in the sales day book, but was posted to Meshack Co. Ltd account as TShs 10,600 while total sales of the month were over casted by TShs 1,000.

| Sales-cash | 344,890 |

| Credit | 268,187 |

| Purchases- cash . | 14,440 |

| Credit . | 496,600 |

| Total receipt from customers | 600,570 |

- Goods purchased from Calorine Maguu & Sons for TShs 15,050 recorded in the purchase’s day book from the invoice as TShs 15,500 and posted to the purchases account and Calorine Maguu & Sons in the ledger accordingly.

- A cash purchases of tools TShs 12,300 from Goodone hardware a supplier were entered in the cash book only.

- A page in the purchases book was overacted by TShs 12,000.

- The sales account was under casted by TShs 4,000.

- The petty cash book balance of TShs 7,100 were omitted from the trial balance.

- N.Cheupe was credited with TShs 7,740 instead of TShs 7,470.

- A sale of TShs 14,000 was incorrectly credited to K. Haonga a debtor

- A payment of TShs 9,200 made for carriage on purchases was posted to carriage inwards account.

- A cash discount of TShs 2,000 allowed to a debtor was correctly posted to his Account but was credited to discount received account.

8. From the following particular extracted from the book of trader. Prepare total accounts receivable and total accounts payable for the year ended 30th November 2022.

- Balance on 1st January 2022

| Sales-cash | 344,890 |

| Credit | 268,187 |

| Purchases- cash | 14,440 |

| Credit | 496,600 |

| Total receipt from customers | 600,570 |

| Total payment to suppliers | 503,970 |

| Discount Allowed (all to credit customers) | 5,520 |

| Discount received (all from credit suppliers) | 3,510 |

| Refund given to cash customers | 5,070 |

| Balance in the sales ledger set off against balance in the purchase’s ledger | 70 |

| Bad Debts written off | 780 |

| Increase in the allowance for doubtful debts | 90 |

| Credit note issued to credit customers | 4,140 |

| Credit note received from credit suppliers | 1,480 |

- According to the Audited Financial Statement for the previous year accounts receivable and accounts payable as at 1st December 2021 were TShs 26,555 and 43,450 respectively.

9. Naweza Company Limited own a manufacturing industry which had the following record for the year ended at 31st December 2021

Inventory (stock) at 1st January 2021 Tzs

Direct materials . . . . . . . . . 10,000

Work in progress . . . . . . . . 38,000

Finished goods . . . . . . . 40,000

Purchases (Direct materials) . . . . . . 140,000

Carriage inwards . . . . . 24,000

Direct wages . . . . . . . . . 222,000

Direct expenses (patent royalties) . . . . . . . . 46,000

Indirect matereials . . . . . . . 45,000

Indirect labour . . . . . . . 72,000

Rent: Factory . . . . . . 100,000

Office . . . . . . . . 90,000

Total payment to suppliers. . . . . . . 503,970

Discount Allowed (all to credit customers). . . . 5,520

Discount received (all from credit suppliers). . . . . . . 3,510

Refund given to cash customers . . . . 5,070

Heating, lighting and power: Factory . . . . . . 45,000

Office . . . . . . . . 35,000

Sales . . . . . 1,300,000

Administration salaries and wages . . . . . 175,000

- Additional Information

a) Inventory (stock) at 31st December 2021 was as follows

- Direct materials TShs 18,000

- Work in progress TShs 20,000 Finished goods TShs 60,000

b) Depreciation is to be provided on noncurrent assets as follows;

- Factory building TShs 20,000

- Factory machinery TShs 36,000 Office equipment TShs 24,000

c) Factory profit is to be calculated at 15% on the cost of production

You are required to prepare;

- Statement of manufacturing cost for the year ended 31st December 2021

- Income statement for the year ended 31st December 2021

FORM FOUR BKEEPING EXAM SERIES 250

FORM FOUR BKEEPING EXAM SERIES 250

OFFICE OF THE PRESIDENT, REGIONAL ADMINISTRATION AND LOCAL GOVERNMENT

SECONDARY EXAMINATION SERIES

MID TERM EXAMINATION-MARCH-APRIL-2025

BOOK-KEEPING FORM FOUR

INSTRUCTIONS

1. This paper consists of section A, B and C with a total of seven {7} questions

2. Answer all questions in both sections

3. Time allowed is 2:30 hrs

SECTION A (15 Marks)

1. For each of the following items (i-x) choose the best correct answer from the given alternatives and write its letter on then answer sheet.

i. Business enterprise will not be closed down shortly is known as: A. On going concern concept B. Historical concern concept C. Money measurement concept D. Dual concept E. Matching concept

ii. Government expenditure on items from which the government attains no value are called; A. Development expenditure B. Recurrent expenditure C. Capital expenditure D. Nugatory expenditure E. Revenue expenditure

iii. If a non-trading organization operates a bar of profit purpose which of the following would determine if that activity made a profit or loss. A. Income statement B. Receipt and payment C. Income and expenditure D. Subscription account E. None of the above

iv. The existing provision for bad debts in the books of Anna is Tsh. 5,600 on 31st December, the sundry debtors stood at 98,000; it is the policy of the company to create a provision of bad debts of 12% per annum. What would be the amount to be transferred to income statement? A. 2,450 B. 1,350 C. 4,250 D. 6,160 E. 3,150

v. If total of two trial balance do not agree, the difference must be entered in: A. Real account B. The capital account C. Trading account D. A suspense account E. Debtors account

vi. In triple column cashbook, cash withdraw from bank for office use will appear on:

A. Debit side of the cash book only B. Both side of the cash book C. Credit side of the cash book only D. Discount column E. Discount receiver account

vii. A firm bought a motor car for TZS 70,000; it was expected to be used for 5 years the sold for TZS 45,000. What is the annual amount of depreciation if the straight line method is used. A. TZS 5,000 B. 7,000 C. 7,500 D. 6,750 E. 16,000

viii. If stock at the end of the year is undervalued, gross profit will be: A. Understated B. Overstated C. Only affected next year D. Not affected E. Overvalued

ix. The balances in the purchases ledger usually: A. Contras B. Debit balances C. Normal account balances D. Real account balances E. Credit balances

x. The document issued by a bank to inform its customers of their state affairs is referred to as: A. Cash book B. Cheque book C. Bank statement D. Cheque sheet E. Unpresented cheque

2. Match the explanations of the bank reconciliation concepts in column A with the corresponding phase in column B by writing the letter of the correct response beside the item number in your answer sheet.

SECTION B: (40 Marks)

3. Briefly explain the following terms a. Book keeping b. Double entry system c. Business entity concept d. Trial balance e. Discount allowed

4. (a) The following information was extracted from the final accounts of John Mpatu’s business on 31st July, 2012.

Transactions during the year Shs.

Sales 300,000/=

Purchases 130,000/=

Stock (1/8/2011) 36,000/=

Fixed assets 200,000/=

Current assets 90,000/=

Current liabilities 74,000/=

Total expenses 20,000/=

Stock ( 31/7/2012) 25,000/=

Calculate the following financial ratios:

(i) Markup (Net profit)

(ii) Margin (Gross profit)

(iii) Return on capital

(iv) Working capital ratio

(v) Rate of stock turnover

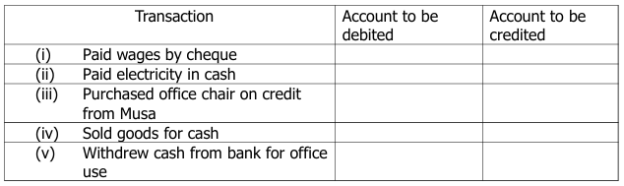

(b) Indicate the accounts to be ‘’Debited”and ‘Credited”from the following transactions.

5. (a) In 2010 Mr. Chipepeto bought a motor car for the cost value of sh. 8,000,000/= with the aim of assisting him in business. But three years later he decided to dispose it for a book value of sh. 6,700,000/=.

i. What is the term used to mean the difference between cost value and book value

ii. Outline four reasons that could be the causes for him to dispose the car for less than the cost value.

(b) The financial year of Duka la Ujamaa ends 31st December each year. At 1st January 2016 Duka la Ujamaa had in use Furniture with atotal accumulated cost of TShs. 135,620 which had been depreciated by a total of Tshs. 81,374. During the year ended 31st December 2016 Duka la Ujamaa purchased new furniture costing Tshs. 47,800 and sold off furniture which had originally cost Tshs. 36,000 and which depreciated by Tshs. 28,224 for Tshs. 5,700. No further purchases or sale of furniture are planned to December.

The policy of the company is to depreciate furniture at 40% using the diminishing balance method. All full year’s deprecation is provided for all furniture in use by the company at the end of each year. Required Prepare the following accounts:

(a) Furniture account

(b) Provision for depreciation account

(c) Furniture disposal account

SECTION C: (45 Marks)

6. The information that follows was extracted from the books of the Nchimba manufactures Ltd as at 31st December 2014.

Additional information

(a) Stock balance as at 31st December 2014 were made up of the following; -

Raw materials TZS 26,000 –

Finished goods TZS 38,000 –

Work in progress TZS 18,000

(b) Lighting, rent and insurance are to apportioned factory 2/3, administration 1/3.

(c) Depreciation on productive and accounting machinery is 10% on cost.

Use the above information to prepare the following;

(i) Statement of manufacturing cost

(ii) Income statement for the year ended 31st December, 2012. 7. On 5th JUNE 2019, M. Halima of Mwanza consigned 1,000 units of goods to J.Manyanya of Arusha, the cost price was Tshs. 800,000.00 M. Halima paid the following expenses;

-Carriage Tshs. 200,000

–Marine insurance Tshs. 80,000

Freight Tshs. 90,000

On 30th June, 2019 J. Manyanya sent an account sale to M.Halima, showing that 600 units were sold for shs. 1,200,000.00 and she incurred the following expenses.

-Carriage Tshs. 150,000

-Import duty Tshs 45,000

-Storage Tshs 50,000

-Commission Tshs 80,000

-Sales expenses Tshs 5,000 Record the above transactions in the books of the consignor, showing the calculation of unsold inventory.

FORM FOUR BKEEPING EXAM SERIES 213

FORM FOUR BKEEPING EXAM SERIES 213

PRESIDENT’S OFFICE, REGIONAL ADMINISTRATION

AND LOCAL GOVERNMENT

SECONDARY EXAMINATION SERIES

COMPETENCY BASED SERIES

BOOK-KEEPING FORM FOUR

MID-TERM EXAMS – AUGUST – 2023

Instructions

1. This paper consists of three sections A, B and C with a total of nine (9) questions.

2. Answer all questions in the sections A and B and two (02) questions from section C.

3. Section A carries 15 marks, section B carries 45 marks and section C carries 40 marks.

4. Cellular phones and any unauthorized materials are not allowed in the examination room.

5. Non programmable calculators may be used.

6. Write your Examination number on every page of your answer booklet(s).

SECTION A (15 Marks)

1. For each of the items (i) - (x) choose the correct answer from among the given alternative and write its letter beside the item number in the answer booklet provided

i. Tshs 500 cash taken from the cash till and banked is entered

A. Debit cash column Tshs. 500 : Credit bank column Tshs. 500

B. Debit bank column Tshs. 500 :Credit cash column Tshs. 500

C. Debit bank column Tshs. 500 : Credit bank column Tshs. 500

D. Debit cash column Tshs. 500: Credit cash column Tshs. 500

E. Debit bank column Tshs. 500

ii. The capital in the business at start of the year was Tshs. 120,000. At the end of the year was Tshs. 142,000. Drawing was Tshs. 1,000 per month. What was the net profit for the year?

A. Tshs. 21,000

B. TShs. 35,000

C. TShs. 22,000

D. TShs. 34,000

E. TShs. 23,000

iii. If a non-trading organization operates a bar for profit purpose which of the following would determine if that activity made a profit or loss

A. Receipts and payments account

B. Subscription account

C. Income statement

D. receipts and expenditure statement

E. Statement of financial position

iv. A business has the cost of goods sold worth TShs. 150,000 and the mark-up of 40%. Calculate the amount of sales for the business

A. TShs. 210,000

B. TShs. 90,000

C. TShs. 102,000

D. Tshs. 150,000

E. TShs 60,000

v. When comparing the performance of individual departments, which of the following statement should be compiled?

A. Department account

B. Statement of financial position

C. Departmental current account

D. Departmental income statement

E. departmental income and expenditure

vi. Kulwa and Dotto share profits and losses in the ratio 3:2. Their partnership recorded net profit of Tshs 1,400, interest on capital Tshs 420, partner’s salaries Tshs 100 and drawings TShs 280. Determine Dotto's share of the profit

A. 840

B. 650

C. 506

D. 464

E. 560

vii. When customer return goods previous sold to him, the shopkeeper will use a document called

A. Credit note

B. Order note

C. Invoice

D. Debit note

E. Purchases order

viii. The following are the source of documents

A. Cheque, invoice, cheque paid

B. Invoice, cash receipts, debit note

C. Sales, credit note, cheque

D. Credit note, debit note, cash

E. purchases, cash, cheque paid

ix. Which of the following is not correct about the petty cashbook?

A. It reduce the number of entries in the norminal ledger

B. The cash spent every month is fixed

C. Cash spent is reimbursed every end of period

D. Petty cashier receives cash from chief cashier

E. Cash spent is reimbursed at the end of the year

x. In government accounting a term family is referred to

A. Mother, wife and children

B. All relatives

C. Wife and children

D. Father, wife and children

E. Mother, father, wife and children

2. Match the explanation of adjustments entries in column A with the corresponding names in column B by writing the letter of the correct response beside the item number in your answer booklet

|

| COLUMN A | COLUMN B |

|

| (i) The expenses that the business has incurred but not yet paid for at the end of accounting period (ii) The amount of revenue that business expects to receive but has not yet been received at the end of accounting period (iii)The expenses which has been paid in advance, the benefits from which will be received in the next period (iv)The amount of revenue which has already been received in the current accounting but related to the following financial year (v)The commulative sum of all depreciation expenses recorded for an asset | A. Prepaid income B. Accumulated depreciation C. Revenue expenditure D. Accrued expenses E. Prepaid expenses F. Accrued income G. depreciation H. Accrual basis |

SECTION B (45 Marks)

3. MASSOUD who owned a retailer business, is not aware of accounting concepts and principles, explain to him the following concepts so that he can understand and apply in his business

i. Money measurement concept

ii. Business entity concept

iii. Historical cost concept

iv. Dual aspect concept

v. Going concern concept

4. Magwe company Traders failed to prepare correct trial balance as seen below You as a student who is expected to sit for National Examination this year 2023.Assist Magwe Co. Traders to prepare correct trial balance basing to accounting principles and concepts

| S/N | PARTICULARS | FOLIO | DEBIT | CREDIT |

| 1 | Wages |

| 2,500 |

|

| .2 | Stock |

|

| 3,500 |

| 3 | Creditors |

| 10,000 |

|

| 4 | Capital |

| 26,000 |

|

| 5 | Water bills |

| 15,000 |

|

| 6 | Discount allowed |

|

| 4,000 |

| 7 | Interest received |

|

| 6,000 |

| 8 | General expenses |

|

| 1,000 |

| 9 | Discount received |

| 7,200 |

|

| 10 | Insurance |

| 8,000 |

|

| 11 | Machine |

|

| 9,500 |

| 12 | Land |

| 7,800 |

|

| 13 | Debtors |

| 2,300 |

|

| 14 | Maintenance of machines |

|

| 6,500 |

| 15 | Advertising |

|

| 1,800 |

| 16 | Sales |

| 5,000 |

|

| 17 | Purchases |

| 7,000 |

|

| 18 | Loan from Said |

|

| 36,600 |

| 19 | Cash at Bank |

|

| 21,900 |

|

|

|

| 90,800 | 90,800 |

5. The following transactions were obtained from the books Bonge Motor cycle spare parts for the month of September 2016

2nd Sold the following to Zuberi on credit

20 tyres @ TShs 30,000 and 6 boxes of oil @ TShs 10,000, less 20% discount

8th Sold on credit to Mussa

16 boxes of bulbs @ TShs 10,000 and 10 side mirrors @ TShs 12,000 less 15% discount

19th Credit to A. Mpili TShs 24,000

25th Sold on credit to Mazengo

7 used motorcycles @ TShs 100,000 and 14 boxes of rubber @ TShs 15,000 less 25% discount

28th sold on credit spare parts to Josky TShs 30,000

Required

Enter the above transactions in the sales Journal

6. You are well experienced and good book keeper , identify five (5) challenges facing the government accounting system in Tanzania

SECTION C (40 Marks)

7. From the following transaction prepare the suspense Account and pass the Journal entries to rectify the following errors. Assuming that at the end of the trading period it was discovered that there was a difference of TShs 35,670 which was debited to the suspense account

a) TShs 17,500 paid in cash for new electronic typewriter had been charged to office expenses account

b) Drawing amounting worth TShs 12,500 by cheque were completely omitted from the books

c) A purchases of goods from M. Batanga for TShs 25,000 were credited to the account of M. Batanga

d) Sales of goods worth TShs 9,600 made to Meshack Co. Ltd account was correctly entered in the sales day book, but was posted to Meshack Co. Ltd account as TShs 10,600 while total sales of the month were over casted by

TShs 1,000

e) Goods purchased from Calorine Maguu & Sons for TShs 15,050 recorded in the purchases day book from the invoice as TShs 15,500 and posted to the purchases account and Calorine Maguu & Sons in the ledger accordingly

f) A cash purchases of tools TShs 12,300 from Goodone hardware a supplier were entered in the cash book only

g) A page in the purchases book was overacted by TShs 12,000

h) the sales account was under casted by TShs 4,000

i) The petty cash book balance of TShs 7,100 were omitted from the trial balance

j) N.Cheupe was credited with TShs 7,740 instead of TShs 7,470

k) A sale of TShs 14,000 was incorrectly credited to K. Haonga a debtor

l) A payment of TShs 9,200 made for carriage on purchases was posted to carriage inwards account

m) A cash discount of TShs 2,000 allowed to a debtor was correctly posted to his Account but was credited to discount received account.

8. From the following particular extracted from the book of trader. Prepare total accounts receivable and total accounts payable for the year ended 30th November

2022 Tzs

Balance on 1st January 2022

| Sales-cash............................................................... | 344,890 | |

| - Credit........................................................... | 268,187 | |

| Purchases- cash..................................................... | 14,440 | |

| - Credit................................................. | 496,600 | |

| Total receipt from customers ................................. | 600,570 | |

| Total payment to suppliers ...................................... | 503,970 |

|

| Discount Allowed (all to credit customers)................ | 5,520 |

|

| Discount received (all from credit suppliers)............ | 3,510 |

|

| Refund given to cash customers ............................ | 5,070 |

|

Balance in the sales ledger set off against balance in the purchases ledger ....70

Bad Debts written off................................................. 780

Increase in the allowance for doubtful debts........... 90

Credit note issued to credit customers..................... 4,140

Credit note received from credit suppliers .............. 1,480

According to the Audited Financial Statement for the previous year accounts receivable and accounts payable as at 1st December 2021 were TShs 26,555 and 43,450 respectively.

9. Naweza Company Limited own a manufacturing industry which had the following record for the year ended at 31st December 2021

Inventory (stock) at 1st January 2021 Tzs

| Direct materials ....................................................... | 10,000 |

| Work in progress .................................................... | 38,000 |

| Finished goods ..................................................... | 40,000 |

| Purchases ( Direct materials) ................................. | 140,000 |

| Carriage inwards ..................................................... | 24,000 |

| Direct wages ............................................................ | 222,000 |

| Direct expenses ( patent royalities ) ......................... | 46,000 |

| Indirect matereials ................................................... | 45,000 |

| Indirect labour .......................................................... | 72,000 |

| Rent : Factory ........................................................... | 100,000 |

| : Office ............................................................. | 90,000 |

| Heating, lighting and power :Factory ........................ | 45,000 |

| Office ............................ | 35,000 |

| Sales .......................................................................... | 1,300,000 |

| Administration salaries and wages ............................. | 175,000 |

Additional Information

a) Inventory (stock) at 31st December 2021 was as follows

Direct materials TShs 18,000

Work in progress TShs 20,000

Finished goods TShs 60,000

b) Depreciation is to be provided on noncurrent assets as follows;

Factory building TShs 20,000

Factory machinery TShs 36,000 Office equipment TShs 24,000

c) Factory profit is to be calculated at 15% on the cost of production

You are required to prepare;

i. Statement of manufacturing cost for the year ended 31st December 2021

ii. Income statement for the year ended 31st December 2021

FORM FOUR BKEEPING EXAM SERIES 168

FORM FOUR BKEEPING EXAM SERIES 168

PRESIDENT OFFICE REGIONAL ADMINISTRATION AND LOCAL GOVERNMENT

SECONDARY EXAMINATION SERIES

FORM FOUR MID TERM TEST MARCH 2023

062 BOOK KEEPING

TIME: 3:00 HOURS.

INSTRUCTIONS.

1. This paper consists of section A, B and C with a total of nine (09) questions.

2. Answer all questions in section A and B and two (02) questions from section C.

3. Non programmable calculators may be used.

4. Cellular phones and any unauthorized materials are not allowed in the examination room.

5. Write your Examination Number on every page of your answer sheet(s).

SECTION A (20 Marks)

Answer all questions in this section.

1. For each of the items (i) – (xv), choose the correct answer among the given alternatives and write its letter beside the item number.

(i) If petty cashier had the balance of TZS 12,000 on 1st January, then on 2nd January received TZS 32,000 to restore the imprest. How much was the desired cash float?

- TZS 20,000

- TZS 24,000

- TZS 44,000

- TZS 32,000

- TZS 12,000

(ii) Making the second entry of double entry system is known as

- Posting

- Recording

- Transaction

- Narrating

- Journalizing

(iii) If the opening capital was TZS 35,000, closing capital TZS 29,700 and drawings were TZS 8,600,

- The loss for the year was TZS 3,300

- The profit for the year was TZS 3,300

- The loss for the year was TZS 5,300

- The profit for the year was TZS 21,100

- The profit for the year was TZS 26,400

(iv) Which one of the following would not be taken into account when calculating working capital?

- Cash

- Debtors

- Loan from bank

- Motor vehicles

- Creditors

(v) A separate fund which is controlled by accounting officer is known as.

- Warrant of fund

- Vote

- Consolidated fund

- Special fund

- Virement

(vi) Which of the following best describes the meaning of trial balance?

- It is a list of balances on the books

- Shows the financial position of the business

- It is a special account.

- It shows total receipts and total payments plus balance.

- It shows all the entries in the books.

(vii) Amina of Iringa consigned 200 cases of goods to Halima of Kigoma. Then Halima is

- Principal

- Consignor

- Partner

- Agent

- Consignee

(viii) Errors are corrected via the journal because

- It provides a good record explaining the double entry records

- It is much easier to do so

- It saves entering them in the ledger

- It saves the book keeper time

- It is a special journal.

(ix) The sales day book best described as

- Containing real account

- A list of credit sales

- Containing customers’ accounts

- Part of double entry system

- A list of cash sales.

(x) When there is partnership agreements profit and losses must be shared

- Equally

- In the same proportion as capital

- In the same proportion as current account

- Equally after adjustments

- According to partnership deeds.

(xi) Bank reconciliation statement is?

- A process of rectifying the difference between cash book and bank statement

- A statement which is prepared in order to rectify the difference between cash book and bank statement

- A summary of customer’s bank account

- An instructions made by the customer to the bank to pay specific amount of money to a specific persons on a specific dates.

- Usually done by the customers.

(xii) Which one of the following does not appear in a statement of manufacturing cost?

- Depreciation on factory machinery

- Depreciation on office equipment

- Royalties

- Foremen’s wages

- Factory power

(xiii) An audit which cover only part of trading period is called

- Procedural audit

- Final audit

- Management audit

- Balance sheet audit

- Interim audit

(xiv) Costs of building warehouse would be classified as

- Capital receipts

- Revenue expenditure

- Revenue receipts

- Recurrent expenditure

- Capital expenditure.

(xv) A club’s receipts and payments account is similar to a firms’:

- Balance Sheet

- Capital account

- Trading, and Profit and loss account

- Cash Book

- Trial balance

2. Choose the correct term from LIST B which matches with the explanation in

LIST A and write its letter in the answer sheet provided.

| LIST A | LIST B |

| i. A ledger for impersonal accounts ii. A ledger for debtors accounts iii. A ledger for creditors accounts iv. A ledger for capital and drawing accounts v. A ledger for cash and bank accounts |

|

SECTION B (40 Marks)

Answer all questions in this section

3. Briefly explain the following accounting concepts:

(a) Business entity

(b) Money measurement concept

(c) Accruals

(d) Going concern

(e) Dual aspect

4. A partnership may be formed through an oral or a written legal agreement among the partners. Suppose there is no written partnership agreement, explain briefly five provisions of the Partnership Act that would govern the operations of the partnership

5. From the following information extracted from the books of MAKINIKIA, you are required to prepare the appropriate control account.

2010 August 1

Sales ledger balances -

- Debit 11,448

- Credit 66

2010 August 31 Transactions for the month

- Cash received 312

- Cheque received 18,717

- Credit sales 21,270

- Bad debts written off 918

- Discount allowed 894

- Returns inwards 1,992

- Refund to overpaid customers 111

- Dishonored cheque 87

- Interests charged by us on overdue debt 150

At the end of the month:

Sales ledger balances -

- Debit 10,287

- Credit 120

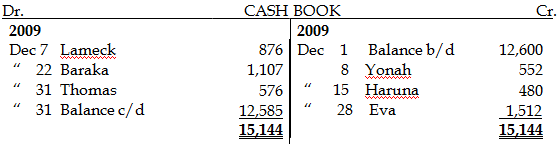

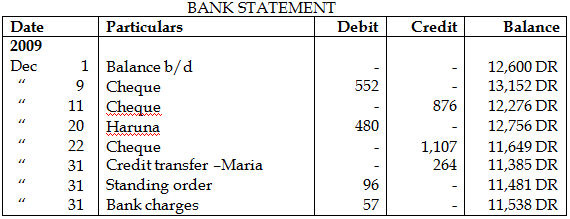

6. The following are the extracts from the cash book and bank statement of Peter.

You are required to:

(a) Adjust the cash book

(b) Draw up bank reconciliation statement as on 31st December 2009.

| |

|

SECTION C (40 Marks)

Answer only two (2) questions in this section

7. (a) Shirima Traders has two departments A and B some items of income and expenditure are allocated directly to the two departments. The remaining expenses are to be allocated to each department in the ratio provided, except Rent & rate and Heat & light should be apportioned equally:

Department A – two – fifths

Department B – three – fifths

You are required to draw up Departmental Income Statement to show the gross and net profit for each department.

| Details | Department A (TZS) | Department B (TZS) |

| Opening Stock | 8,000 | 12,000 |

| Purchases | 16,000 | 20,000 |

| Closing Stock | 9,000 | 4,000 |

| Sales | 38,000 | 52,000 |

| Wages & Salaries | 15,000 | 23,000 |

Expenses to be allocated between departments are:

- Heat and light TZS 4,000

- Rent and rates TZS 1,200

- Carriage Inwards TZS 1,000

- Carriage outwards TZS 500

- Office expenses TZS 2,000

(b) Record the following transactions in the cash account of Mayele.

2022 Jan, 1. Commenced business with capital …………. 50,000

2. Bought goods for cash………………………… 40,000

4. Sold goods on credit to Masi ……………… 15,000

5. Sold goods to Suma and Company …………. 20,000

12. Sold goods for cash ………………………… 25,000

15. Bought goods from Bite …………………… 10,000

16. Paid wages in cash ………………………… 9,000

20. Bought furniture for cash…………………… 11,500

25. Paid transport charges in cash..……………… 1,000

29. Paid rent in cash……………………………. 500

8. Somi, Mumi, and Jessa are partners sharing profits and losses in the ratio of 2:2:1 respectively. Somi draws TZS 10,000 every month, and Mumi and Jessa TZS 8,000 each every month and interest on drawings was calculated to TZS 6,000 , TZS 4,800 and TZS 4,800 respectively. Also charging interest on capital at 5 percent per year. A partnership salary of TZS 80,000 to Mumi per year and TZS 60,000 to Jessa per year. The profit for the year ending December 31st 2020 was TZS 1,152,000.

You are required to write up profit and loss appropriation account and current account.

Given the following additional information.

| Details | Somi | Mumi | Jessa |

| Capital (1.1.2020) Current accounts (1.1.2020) | TZS 1,000,000 90,000(Cr) | TZS 800,000 50,000(Dr) | TZS 300,000 10,000(Cr) |

9. The following is a trial balance of Mr. Masantula for the year ended 31st December 2020 Mr. Masantula’s Trial Balance as at 31st December 2020

|

Notes at 31/12/2020

i. Inventory of raw materials Tsh 24,000, Inventory of finished goods Tsh

40,000 and Inventory of work in progress Tsh 15,000

ii. Lighting, rent and insurance are to be apportioned: Factory 5/6, Administration 1/6

iii. Depreciation on productive machinery and administration computer at

10% per annum on cost iv. Net profit was Tsh 89,800

Use the given information to prepare the Statement of Manufacturing Cost for the year ending 31st December 2020 and the Statement of Financial Position as at 31st December 2020.

FORM FOUR BKEEPING EXAM SERIES 142

FORM FOUR BKEEPING EXAM SERIES 142

THE PRESIDENT’S OFFICE

MINISTRY OF EDUCATION, REGIONAL ADMINISTRATION AND LOCAL GOVERNMENT

COMPETENCE BASED SECONDARY EXAMINATION SERIES

BOOK KEEPING ANNUAL EXAMINATIONS

FORM FOUR-2022

INSTRUCTIONS

- This paper consists of section A, B and C with a total of nine (9) questions.

- Answer all the questions in section A and B and two (20 questions from section C.

- Section A carries Twenty (20) marks, section B and C carry forty (40) marks each.

- Non-programmable calculators may be used.

- All communication devices, programmable calculators and any unauthorized materials are not allowed in the examination room.

- Write your Exam ination Number on every page of your answer booklet (s)

SECTION A (20 Marks)

Answer all questions in this section

- For each of the following items (i) – (xv), choose the correct answer from the given alternatives and write its letter beside the item number in the answer booklet provided.

- The profit which expressed as a fraction or percentage of the selling price is known as

- Net profit

- Margin

- Markup

- Rate of stock turn over

- Non-of the above

- A customer buys 100 goods of Tzs 5000 each and has been given a 25% trade discount if he pays within 30 days. What amount would he pays within discounting periods?

- Tzs 735000

- Tzs 573000

- Tzs 125000

- Tzs 625000

- Tzs 375000

- In the books of consignor the balance of the consignment stock account would be shown

- As an asset in the balance sheet

- As a liability in the balance sheet

- On the credit side of trading account

- On the debit side of consignment account

- Consignors account

- Which of the following is a capital expenditure?

- Rent

- Wages

- Salaries

- Fire insurance

- Motor van

- How could a purchase of a non-current asset by cheque affect the balance sheet

- By decreasing non-current assets accounts and decrease bank account

- By increasing Bank account and decrease Bank Account?

- By increasing non current asset account and decreasing cash account

- By increasing non-current asset account and decreasing bank account

- What is the purpose of the provision for doubtful debts account in the business?

- To write off bad debts

- To record all possible bad debts

- To recover all bad debts

- To provide debtor discounts

- To record bad allowance

- A cheque which is not accepted for payment by the bank due to insufficient fund in the drawers bank account is referred to as

- Dishonoured cheque

- Outstanding cheque

- Bank lodgment

- Unrecorded cheque

- Stale cheque

- Which one of the following would you not take into account in calculating working capital?

- Cash

- Debtors

- Amount at bank

- Creditors

- Motor vehicles

- In the books of consignors the acceptance of bills of exchange by the consignee will be credited to

- Consignment account

- Consignees account

- Bill receivable account

- Bill payable account

- Trading account

- In case of del-credere commission, the liability for bad debts is a burden to?

- Consignees

- Consignor

- Customer

- Profit and loss account

- Consumer

- X and Y are partners in a firm sharing profit and losses in the ratio of 3:1. Z is admitted as a partner who pays Tzs 4000/= as a goodwill. The profit sharing ratio is 2:1:1. Then goodwill is credited to:

- Y’s capital 4000/=

- X’s capital 4000/=

- X’s capital 3000/= and Y’ s capital 1000/=

- Profit and loss Appropriation account

- Revaluation account

- Where will you record interest on drawing

- Debit side of profit and loss appropriation account

- Credit side of profit and loss appropriation account

- Credit side of profit and loss accounts

- Credit side of capital/current account only

- Partners capital account

- In the absence of partner’s agreements, partners are entitled to

- Salary

- Commission

- Interest on loan and advances

- Profit share in capital ratio

- Share profit equally

- The users of accounting data;

- Farmer, teacher and banker

- Doctors, bankers and government

- TRA, School and Hospitals

- Trader, bankers and government

- Schools, Market and head of Dept

- The asset are arranged in order of liquidity which is the descending order in which current asset should be shown in the balance sheet.

- Inventory, account receivable, bank, cash

- Inventory, account receivable, cash, bank

- Account receivable, inventory, bank, cash

- Cash, bank, account receivable, inventory

- Bank, Inventory, cash, account receivable

- Match the explanations of Auditing concept in Column A with the corresponding terms in Column B by writing the letter of the correct response beside the items number in the answer booklet provided.

| COLUMN A | COLUMN B |

|

|

SECTION B (40 MARKS)

Answer all questions in this section

- Book keeping involves the recording on a daily basis of a company’s financial transactions whether on single entry system or double entry system and because of book keeping, companies are able to track all financial information on its books to make key operating, investing, and financial information on its books to make key operating, investing, and financing decisions. Outline four reasons stating why single entry system is not important in book keeping.

- A trial balance was extracted from books of C. Mtumzima and it was found that the debit side exceeded the credit side by TZS 1,000,000/=. This amount was recorded in the suspense Account. The following errors were later discovered and corrected.

- Purchases were over casted llater by TZS 400,000/=

- An amount paid by T.Lulanga was debited to the control Account as TZS 870,000/= instead of TZS 780,000/=

- Sales were under-added by TZS 510,000/=

Required:

- Open Journal entries to rectify above errors

- Write up the suspense Account as it would appear in C.Mtumzima’s Ledger

- Shedrack Traders had the following assets and liabilities on the date shown:

01.01.202031.12.2020

Premises 14,500 14,500

Motor cars 2,800 1,800

Furniture 3,500 3,200

Stock in Trade 11,200 13,100

Trade debtors 10,900 11,400

Trade creditors 14,600 17,200

Cash at bank and in hand 1,330 3,980

Prepaid expenses 670 1,120

Accrued expenses 1,300 600

Additional information

During 2020 he withdrew TZS 300 per month from the business bank account for his personal use. On 4 July 2020 he sold his personal car for TZS 12,000 and paid the proceeds into the business bank account

Required:

Calculate the net profit or loss made by Shedrack Traders in 2020.

- On 31st December 2017, the cash book balance of Bonge Traders was TZS 253,700/= where the bank statement showed a credit balance of TZS 256,700/= In comparing these two balances, the following were discovered;

Cheques not yet presented for payment TZS 123,400/=

Cheques paid into the bank but not yet credited by the bank account TZS 121,600/=

Items shown in the bank statement but not yet entered in the cash book were as follows

- Bank charges TZS 2,400/=

- Standing order TZS 4,600/=

- Dividends collected by the bank TZS 8,200/=

Required:

Prepare a bank reconciliation statement starting with balance as per bank statement. (Do not update the cash book)

SECTION C (40 Marks)

Answer two (2) questions from this section

- (a)Majani and Master J enter into a Joint venture to share profit losses equally resulting from dealings in second-hand digital TVs, both parties taken an active role in the business, each recording his own transactions. They have no Joint Bank Account.

2021

July 1: Majani busy four TVs for a total of TZS __________ 110,000/=

July 3: Majani pays for repairs TZS _______ 84,000/=

July 4: Master J pays office Rent TZS 30,000/= and advertising TZS 9,000/=

July 6: Master J pays for Packing materials ________ TZS 3,400/=

July 7: Master J buys a TV in excellent condition for __________ TZS 60,000/=

July 31: Majani sells the five (5) TVS to various customers, the sales being competed on this date and totaling TZS 310,000/=

Required:

- Show the relevant Accounts in the books of co-ventures

- Memorandum joint venture account

(b) Given the table below;

| DATE | ACCOUNTS RECEIVABLE | PROVISION FOR BAD DEBITS 2% ON DEBTORS |

| 2018 | 500,000 | 2 |

| 2019 | 400,000 | 2 |

| 2020 | 600,000 | 2 |

Prepare

- Provision for bad debts account

- Income statement

- Statement of financial position

- On 6th June 2020, Bagamerchant in Congo sent a consignment of 500 cases of goofs to Kungu, his agent in Babati Tanzania. The goods had Baga TZS 4000/= per case and paid transport and insurance amounted to TZS 50,000/=

Baga’s Accounting period ended on 31st December 2020, and Kungu sent him an Interim Account sales made up to that date. It was disclosed that 400 cases had been sold for TZS 6000/= per case and import duty TZS 192,000/= and distribution expenses TZS 20,000/= had been paid. Commission at 5% on sales plus 2% Del-credere was charged.

On 10th March 2021, Baga received the final Account sales showing that the remainder of the consignment had been sold for TZS 5000/= per case, distribution charges TZS 32,000/= had been paid and a commission was deducted. A cheque was enclosed for the Balance of Baga.

Required:

- Prepare necessary accounts in the books of Baga for year 2020 and 2021.

- Account sales

- Marenga company ltd was formed on 1st January 2015 and the following information is available for its first four years of operation

2015: Bought motor car costing shs 2,000,000 on 1.7.2017

2018: sold motor car which was bought for sh 6,000,000 on 1.1.2015 for the sum of 3,000,000 on 30th September 2018

Marengacompany ltd depreciates its motor car at the rate of 10% per annum, reducing balance method for each month of ownership. The accounting period for the company ltd endes in December each year.

Required

For each of the year 2016, 2017 and 2018, prepare the following accounts/statements

- Motor car account

- Provision for depreciation account

- Disposal account

- Income statement

- Statement of financial position

FORM FOUR BKEEPING EXAM SERIES 134

FORM FOUR BKEEPING EXAM SERIES 134

THE PRESIDENT’S OFFICE MINISTRY OF EDUCATION, REGIONAL ADMINISTRATION AND LOCAL GOVERNMENT

COMPETENCY BASED SECONDARY EXAMINATION SERIES

BOOK KEEPING

FORM FOUR- SEPT 2022

INSTRUCTIONS

- This paper consist of three section A, B and C

- Answer all questions in section A and B and only two (2) questions in section C

- The use of Scientific Non programmable calculators is allowed in the examination room

- Write your Examination Number in every page of your answer sheet (s)

SECTION A (20 MARKS)

Answer all questions in this section

- For each of the items (i) – (xv), choose the correct answer from the given alternatives and write its letter beside the item number in the answer sheet provided.

- The cash payment of TZS 4,000 to Biriani will appear as

- Debit Cash account, Credit Biriani account

- Debit Biriani account, Credit Bank account

- Credit Cash account, Debit Bank account

- Debit Biriani account, Credit Purchases account

- A balance of an account can defined as the

- Balance carried down

- Difference between two sides of an account

- Total amount of debit and credit sides

- Balance brought down

- Balancing figure of an account

- “True and Fair view” state of affairs is a conclusive word in audit report. According to the auditor, it means;

- Financial statements are true and accurate

- Financial statements are fairly prepared

- Financial statements are prepared following the double entry system

- Financial statements belong to a True and Fair view of a firm.

- Financial statements are accurately prepared

- In a partnership which of the following statements is correct?

- Current account is used where fluctuating capital account is adopted

- Fixed capital account is used where appropriation account is not opened

- Fixed capital account is prepared where there is no partnership agreement

- Current account is prepared where there is no partnership agreement

- When fixed capital account is maintained current account should be opened.

- Which of the following will happen if TZS 6,000 will be added to Machinery repair instead of being added to Non-current asset?

- Gross profit will not be affected

- Gross profit would be affected

- Gross profit and net profit would be affected

- Net profit would be affected

- Net profit would not be affected

- What is meant by the term revenue expenditure?

- The extra capital paid by the proprietor

- Money spent on non-current asset

- The cost of running the business on day to day basis.

- Money of painting a non-current asset

- Cost of buying a machinery

- The following are source domestics;

- Sales, credit note, cheque

- Cheque, invoices, cash

- Invoice, receipt, debit note

- Credit note, debit note, cash

- Bank, invoices, credit note

- A firm bought machinery for TZS 50,000 which had a scrap value of TZS 5,000, and useful life of 5 years. What would be the depreciation expenses if straight line method is used?

- TZS 9,000

- TZS 11,000

- TZS 10,000

- TZS 5,000

- TZS 11,500

- Cash float of 2,560/= is desired if 2,000/= is spent if the period now much will be reimbursed at the end of the period?

- 560

- 4000

- 2000

- 2560

- 4560

- Which among the following adjustment is treated as current assets in the preparation of statement of financial position?

- Prepaid income

- Accrued expense

- Accrued revenue

- Outstanding expenses

- Unearned revenue.

- Which of the following depreciation methods uses the reduced value to compute the depreciation of non-current assets?

- Straight line method

- Sum of the years digits method

- Unit of output method

- Diminishing balance method

- Revaluation method

- Which of the following are the examples of revenue expenditure?

- Purchases of furniture and payment for electricity bill

- Repair of van and petrol costs for van

- Buying machinery and paying for installation costs

- Electricity coasts of using machinery and buying van

- Buying a van and petrol costs

- If the cost of goods sold is TZS 16,000 and the profit margin is 20%, determine the amount of sales.

- TZS 3,200

- TZS 20,000

- TZS 16,800

- TZS 24,000

- TZS 12,800

- Which of the following best describe a trial balance?

- Shows the financial position of a business

- It is a special account

- Shows all the entries in the same place

- It is a list of balances on the same place

- It is used to calculate profit

- The main purpose of manufacturing statement is to deduce

- The cost of production

- Cost of raw materials available for use

- Prime cost

- Factory profit

- The cost of sales

- Match the answer in LIST B with the response in LIST A and write the letter of the most correct response.

| LIST A | LIST B |

|

|

SECTION B (40 MARKS)

Answer all questions in this section

- (a)With example explain six (6) errors which do not revealed by trial balance,

(b) Give out four (4) differences between consignment and joint venture

- (a)Outline the reasons causing the differences between bank balance on cashbook and bank statement (five reasons)

(b)Mention any five (05) users of financial statements

- (a)The following table shows information relates to the Soccer City club subscriptions for the year 2015. You are required to prepare subscription account for the year ended 31st December 2015

| Item | 1st January 2015 | 31st December 2015 |

| Subscription in arrears | Tshs 4,000 | Tshs 2,100 |

| Subscription in advance | Tshs 1,200 | Tshs 8,900 |

Subscriptions – Received during the year 2015 were Tshs. 48,920/=

(b)You are provided the following information from the books of Kisinda on 30th JUNE 2018. Complete the following table.

|

| ASSETS | CAPITAL | LIABILITIES |

| | 157000 | 86500 | ……….. |

| | ………. | 247000 | 885000 |

| | 273100 | ………. | 63500 |

| | ………… | 381500 | 13430 |

| | 205000 | 176200 | ……… |

- Mtumbadi of Morogoro consigned 2000 cases of Tomatoes to Munyabi of Kibaha at a price of 800/= @case. Mtumbadi incurred the following expenses, packing 4,000/=, freight 30,000/=, export duty 8,000/= and insurance, 7,000/=. Munyabi paid import duty 27,000/=, advertising 9,000/= and carriage on sales 7,000/=. Munyabi has to receive 20% commission plus 10% delcredere commission on sales. Munyabi made the following sales.

- 800 cases sold at a price of 600@

- 400 cases sold at a price of 1,500@

- 400 cases sold at a price of 900 @

The units unsolved were kept by the consignee; the balance was remitted by bank draft

Required: Prepare

- Consignment outward A/C

- Consignment to Munyabi A/C

SECTION C: (40 MARKS)

Answer only Two questions in this section

- Given the following Trial balance of Madulu ltd as on 31st August 2015

| Item | DR TSH | CR TSH |

| Drawing and capital Motor van Purchases and sales Inventory at start Returns Carriage inwards Carriage outwards Wages and salaries Commission discounts Provision for bad debts Premises Bad debts Insurance Rent received Provision for depreciation motor van Debtors and creditors Bank Petty cash | 4,000 30,000 60,000 5,000 6,000 2,000 1,000 8,000

5,000

40,000 800 4,000

10,000

1,200 | 51,900

80,000

3,000

7,000 9,000 600

2,500 2,000

9,000 12,000 |

|

| 177,000 | 177,000 |

Additional information

- Inventory at close Tsh 6,000/=

- Accruals were wages shs 1,500/= and commission Tsh 1,200/=

- Prepayment insurance shs 700/= and Rent receivable Tsh 900/=

- Goods taken by the owner for own use Tsh 400/=

- Provision for bad debts in 5% on debtor

- Depreciate motor van and premises by 10% p.a on cost

Required: From the above transactions found in the books of Maduhu ltd. Prepare

Income statement for the year ended 31st August 1995 and the statement of financial position as to date

- Chama and Bwalya own a retail business in Mwanza. Their retail showroom has three Departments namely X, Y and Z. The following balances were extracted from their books as at the end of their financial year, 31st December, 2020.

| Item | Tshs | Item | Tshs |

| Opening Stock: Department -X -Y -Z Purchases: Department -X -Y -Z

Sales: Department -X -Y -Z

Closing Stock: Departments -X -Y -Z |

75,780 48,000 40,000

281,400 161,200 88,800

360,000 270,000 180,000

90,160 34,960 43,180 | Salaries and wages Advertising Rent Discount allowed Discount Received Sundry expenses Depreciation on Furniture and fittings | 96,000 4,500 21,600 27,000 1,600 24,300

1,500 |

Additional information

- Goods having a transfer price of shs 21,400/= and shs 1,200/= were transferred from Departments X and Y respectively to Department Z

- The various items shall be apportioned among three Departments in the following proportion

| S/N | Item | Depart X | Depart Y | Depart Z |

| | Rent | 2 | 2 | 5 |

| | Salaries and wages | 1 | 1 | 1 |

| | Discount received | 8 | 5 | 3 |

| | Depreciation | 1 | 1 | 1 |

| | All other expenses | On the basis of sales | ||

Required

- Departmental income statement for the year ended 31st December 2020

- Determine the business’ operational result

- Comment on the performance of departmental

- The Trial balance of Awilo a sole trader, taken out on 30th September 2002, Fail to agree. To detect errors, he decided to prepare sales and purchases control accounts from the following information

Tshs

Sales ledge debit balances 1.10.2001. 227,200

Sales ledger credit balances 1.10.2001 420

Purchases ledger debit balances 1.10.2001 1,270

Balances for the year to 30th September 2002

Credit sales 402,120

Cash sale 153,700

Cash purchases 85,600

Credit purchases 160,560

Sales returns 2,120

Purchases returns 4,500

Cash payment to creditors 222,700

Bad debts written off 4,700

Cash received from debtors 411,000

Dishonoured cheque in favour of customers 9,000

Provision for bad debts 4,790

Carriage charged to customers 3,600

Discount allowed 20,110

Legal fees charged to customers 450

Debit balances in sales ledger transferred to purchases ledger 2,000

The lists of balances extracted from the personal ledger were as follows;

Tshs

Debtors: Debit balance 206,160

Credit balances 540

Creditor: Credit balances 83,115

Debit balances 825

Required;

- Prepare control accounts

- State the amount of errors occurred in each account.

FORM FOUR BKEEPING EXAM SERIES 122

FORM FOUR BKEEPING EXAM SERIES 122

THE PRESIDENT’S OFFICE

MINISTRY OF EDUCATION, REGIONAL ADMINISTRATION AND LOCAL GOVERNMENT

COMPETENCE BASED SECONDARY EXAMINATION SERIES

BOOK-KEEPING TERMINAL EXAMINATION

FORM FOUR -2022

Instructions

- This paper consists of sections A, B and C with a total of nine (9) questions.

- Answer all questions in sections A and B and two (2) questions from section C.

- Section A carries twenty (20) marks and section B and C carry forty (40) marks each

- Non programmable calculators may be used.

- Cellular phones and any unauthorised materials are not allowed in the examination room.

- Write your Examination Number on every page of your answer booklet(s).

SECTION A (20 Marks)

Answer all questions in this section.

- Which categories of errors represent errors which do not affect the Trial Balance agreement?

- Errors caused by inaccurate arithmetic operations.

- Errors which cancel out each other in the trial balance.

- Errors caused by omission of a balance of account.

- Errors caused by entering an item once in an account.

- Errors caused by posting an item on a wrong side of an account.

- Costs incurred for machine repairs in accounting for departmental businesses is appropriately apportioned according to

- the value of machinery in each department.

- the value of non-current assets in each department.

- the number of machines in each department.

- the number of machine hours used in each department.

- the floor area occupied by each machine.

- How is the capital for a non-profit making organization described?

- Capital employed fund

- Capital supplied fund

- Accumulated fund

- Gross working capital fund

- Accumulated shares fund

- How would you record the commission due to consignee in the books of the consignee?

- Dr. Consignee's account and Cr. Consignment account

- Dr. Consignment account and Cr. Profit and loss account

- Dr. Profit and loss account and Cr. Consignment account

- Dr. Consignor's account and Cr. Commission Receivable account

- Dr. Goods on consignment account and Cr consignment account

- Amani business had an opuning balance of TZS 12,.500 fnr creditors at the beginning of the year and the closing creditors balances of TZS 21,000 at the year end. During the year, the payment made to creditors amounted to TZS 16,000. Calculate the amount of purchases during the year.

- TZS 33,500

- TZS 27,000

- TZS 16,500

- Tzs 24,500

- TZS 7,500

- During the month of January, a petty cashier was provided with an opening cash float of TZS. 70,000. However, at the end of the same month the closing cash float balance was 15,900. How much should be reimbursed to the cashier at the,end of the month?

- TZS 15,900

- TZS 70,000

- TZS 54,100

- TZS 140,000

- TZS 101,820

- A debit balance of TZS 5 ,000 in a cash account shows that

- cash has been overspent by TZS 5,000.

- TZS 5000 was the total of cash paid out.

- the total of cash received was less than TZS 5,000.

- there was TZS 5,000 cash in hand.

- TZS 5,000 was the total of cash received.

- The act of recording transactions in any subsidiary book is called

- posting.

- double entry system.

- transaction.

- balancing.

- journalizing.

- The primary objective of trial balance is

- to make sure that total amount of debit side and credit side are equal.

- to detect and avoid errors and frauds.

- to prepare trading, profit and loss account and balance sheet.

- to test the arithmetic accuracy of the ledger.

- to prepare suspense account.

- What would you consider to be the main source of government revenues?

- Royalties

- Penalties

- Taxes

- Interest

- Fees

- Which of the following would best describe the use of a control account?

- To check the arithmetical accuracy of ledgers

- To show costs ascertained in the ledgers

- To show allowance given by suppliers

- To check the debit balance of sales account

- To show the direct costs allocated to a section of a business

- How would you categorize the subscription paid in advance in the balance sheet of a non-profit making organization?

- A current liability

- A non-current liability

- A current asset

- A non-current liability

- Accumulated fund

- The term depreciation would best be described as the

- value of money used to replace non-current assets.

- value of non-current assets consumed due to its use.

- gradual increase in value of non-current assets due to its use.

- value of a non-current asset that remains after its use.

- amount incurred to repair the non-current assets

- Which of the following depreciation methods uses the reduced value to compute the depreciation of a non-current asset?

- Straight line method

- Sum of the years digits method

- Diminishing balance method

- Machine hours rate method

- Unit of output method

- Prime cost is obtained as a result of

- Cost of raw materials used plus direct wages and factory overhead cost.

- Cost of raw materials used plus direct wages.

- Factory overhead cost plus direct wages.

- Factory cost of goods manufactured less cost of raw materials used.

- Cost of raw materials used less factory cost of goods manufactured.

2.For each of the items (i) - (v), match the descriptions of the different types of capital in Column A with their corresponding names in Column B by writing the letter of the correct response beside the item number in the answer booklet provided.

| LIST A | LIST B |

|

|

SECTION B (40 Marks)

Answer all questions in this section.

3. Briefly explain the following accounting concepts:

- Business entity

- Money measurement

- Accruals

- Going concern

- Dual aspect

4. A partnership may be formed through an oral or a written legal agreement among the partners. Suppose there is no written partnership agreement, explain briefly five provisions of the Partnership Act that would govern the operations of the partnership.

5.(a)The following information was extracted from the books of Rhombo Traders for the year ending 31st December, 2017

| Purchases | 2,000,000 |

| Stock (1st Jan. 2017) | 150,000 |

| Stock (31st Dec. 2017) | 300,000 |

| Sales | 2,500,000 |

| Expenses | 200,000 |

| Rent received | 100,000 |

| Warehouse wages | 80,000 |

| Carriage inwards | 50,000 |

Using the information provided, calculate:

(i) The value of goods available for sale.

(ii) The gross profit for the year.

(iii) The net profit for the year.

(iv) Rate of stock turnover.

(v) Percentage of expenses over sales

6. On 1st January 2015 Mikuyu Motors Company Ltd purchased Motor Lorry worth TZS 12,000,000. The company used the asset for three years. On 31st December 2017 the lorry was sold for TZS 3,000,000. It is the policy of the company to compute depreciation using straight line method.

Using the information provided, prepare the Motor Lorry and Provision for Depreciation on Motor Lorry Account for the three years ending 31st December 2015, 2016 and 2017.

SECTION C (40 Marks)

Answer two (2) questions from this section.

7. The following is the receipts and payment account of Chamwino social club for the year ending 31st December 2017:

| Dr | Cr | ||

| Details | TZS | Details | TZS |

| Balance b/d | 202,500 | Salaries | 50,000 |

| Subscription: Year 2016 | 40,000 | Printing and postage | 20,000 |

| Year 2017 | 206,000 | General expenses | 7,500 |

| Year 2018 | 60,000 | Drama expenses | 4,500 |

| Donations | 5,400 | Stationery | 1,500 |

| Proceeds of drama | 9,500 | Municipal taxes | 4,000 |

| Sale of waste papers | 4,500 | Charity | 3,500 |

|

|

| Electricity bills | 1,450 |

|

|

|

|

|

Additional Information

- There are 500 members, each paying annual subscription fee of TZS 450.

- TZS 9,000 is still in arrears for the year ended 2016 and it was decided to be written off.

- Buildings stand in the books at TZS 500,000 and are to be depreciated at 5%.

- General expenses of TZS 2,100 for the year have not been paid.

Use the information provided to prepare the following:

- Statement of Affairs at 1stJanuary 2017.

- Subscriptions Account for the year ending 31stbecember 2017.

- Statement of Income and Expenditure for the year ending 31 StDecember 2017.

- Statement of Financial Position for the year ended 31stbecember 2017.

8. MS Annet did not maintain her accounting records on a double entry system. On 31 st December 2018 she supplied the following list of assets and liabilities.

|

| 31st December 2017 | 31stDecember 2018 |

| Premises | 350,000 | 295,000 |

| Furniture | 60,000 | 53,000 |

| Motor van | 18,000 |

|

| Trade debtors | 62,800 | 74,300 |

| Trade creditors | 39,500 | 40,700 |

| Loan from bank | 120,000 |

|

| Salaries due | 92,000 | 75,000 |

| Prepaid insurance | 25 ,ooo | 36,000 |

| Rent received in advance | 40 ,000 | 68,000 |

The following information is also available:

(i)During the year to 31 st December 2018, MS Annett made loan repayment of TZS 100,000.

(ii)MS Annett provides for depreciation on motor vans at 10% per annum.

Prepare the statements of affairs to calculate the opening capital as at 1 st January 2018 and closing capital as at 31 st December 2018.

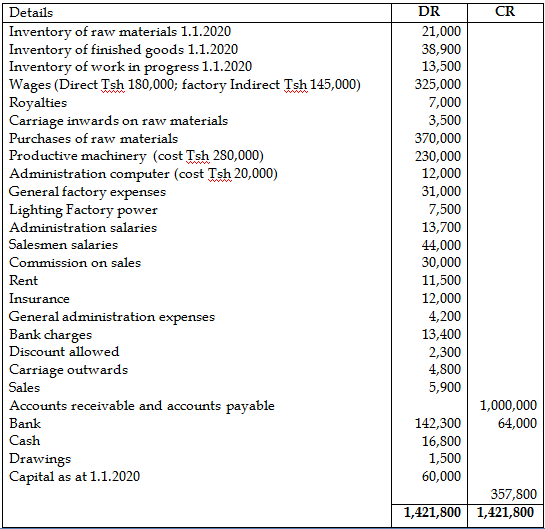

9. The following is a trial balance of Mr Mashamba for the year ended 31st December 2018:

Mr Mashambas Trial Balance as at 31 December 2018

|

| DR | CR |

| Inventory of raw materials 1/1/2018 Inventory of finished goods 1/1/2018 Inventory of work in progress 1/1/2018 wages (Direct 3,600,000 factory indirect TZS 2,900,000) Royalties Carriage inwards on raw materials Purchase of raw materials Machinery and Plant (cost 5,600,000) Office Fixtures (Cost TZS 400,000) Other factory expenses Lighting and heating Factory power and fuel Salaries Sales expenses Commission on sales Rent Insurance General administration expenses Office Rates Discount allowed Carriage outwards

Sales Account receivable & Account payable Cash at Bank Cash in hand

Drawings Capital as at 1/1/2018 | 420,000 778,000 270,000 6,500,000 140,000 70,000 7,400,000 4,600,000 240,000 620,000 150,000 274,000 880,000 600,000 230,000 240,000 84,000 268,000 46,000 96,000 1 18,000

2,846,000 336,000 30,000 1,200,000 | 20,000,000 1,280,000

7,156,000 |

| 28,436,000 | 28,436,000 |

Notes at 31/12/2018:

(i)Inventory of raw materials TZS 480,000, inventory of finished goods TZS 800,000 and inventory of work in progress TZS 300,000.

(ii) Lighting, rent and insurance are to be appoftioned as follows: Factory 5/6, administration 1/6.

(iii) Depreciation on machinery and plant and office fixtures is 10% per annum on cost.

(iv) Net Profit was TZS. 1,796,000.

Use the given information to prepare the Statement of Manufacturing Cost for the year ending 31 st December 2018 and the Statement of Financial Position as at 31st December 2018.

FORM FOUR BKEEPING EXAM SERIES 89

FORM FOUR BKEEPING EXAM SERIES 89

THE UNITED REPUBLIC OF TANZANIA

PRESIDENT’S OFFICE

REGIONAL ADMINISTRATION AND LOCAL GOVERNMENT

FORM FOUR MID TERM EXAMINATION-2021

033/1 BOOK-KEEPING

Time: 3 Hours AUG, 2021

Instructions

- This paper consists of three sections A, B and C with a total of 9 questions.

- Answer all questions in section A and B and only two (2) questions from section C.

- Section A carries twenty (20) marks, section B forty (40) marks and section C forty (40) marks.

- Non programmable calculators may be used.

- Cellular phones, and other authorized materials are not allowed in the examination room.

- Write your examination number on every page of your Answer booklet(s).

SECTION A (20 MARKS)

Answer all questions in this section

- for each of the items (i)-(xv), choose the correct answer from among the given

Alternatives and write its letter beside the item number in the answer sheet provided

- If sales is 20,000 and profit make up is 25%, determine the amount of cost price

A: 13,600 B: 12,000 C: 16,000 D: 12,900 E: 20,600

- Which book of prime entry records the sale or purchase of non-current Assets?

A: General journal B: Sales journal C: Purchases journal D: Cash book E: Sales return day book

- If cash sale amount to Tshs 100,000/= paid direct into the bank account, the correct double entry will be to

A: Debit sales account and credit cash account by sh.100, 000

B: Debit cash account and credit bank account by sh.100, 000

C: Debit bank account and credit sales account by sh.100, 000

D: Debit bank account and credit cash account by sh.100, 000

E: Debit sales account and credit bank account by sh.100, 000

- How much is to be reimbursed if a petty cashier has spent Tsh.189,00/=while his cash float is Tsh.200,000/=

A: Tsh,11,000/= B:Tsh 389,000/= C: Tsh,189,000/= D:Tsh,200,000/= E:Tsh,21,000/=

- Working capital is a term meaning.

- The excess of current liabilities over current liabilities

- The excess of the current assets over the current liabilities

- the excess of the current assets over non-current liabilities

- The excess of current assets over non-current assets.

- The excess of non-current Assets over current liabilities

- Natasha and Ndengwe share profits and losses in the ratio 3:2. Their partnership recorded net profits of shs. 1,400, interest on capital shs. 420, partners’ salaries shs. 100 and drawings shs. 280, Determine Ndengwe’s share of the profits.

- TZS 840 B. TZS 560 C. TZS 464 D. TZS 696 E. TZS 506

- From the following categories of errors, identify the category of errors which affect only one account

A. Casting errors. B. Errors of principle. C. Errors of omission. D. Errors of original entry. E. Errors of commission.

- In the business of C. Sangster, who owns a clothing store, which of the following is the capital expenditure?

- Fixtures and New Van bought B. Shop fixtures bought and wages of assistants C. Wages of assistants and new van bought D. Wages of assistants and Petrol for Van E. Fixtures and salaries.

- Manufacturing account is used to calculate:

- Production cost paid in the year B. Total cost of goods produced C. Production cost of goods completed D. Gross profit on goods sold E. Prime cost of goods manufactured

- Depreciation can be described as the : _______

- Amount spent to buy a non –current asset

- Salvage value of a non-current asset consumed during its period

- Cost of the non-current asset consumed during its period

- Amount of money spent replacing non-current asset

- Cost of old asset plus new assets purchased

- A bank reconciliation statement is a statement:

- Sent by bank when the account are overdrawn

- Drawn to verify cash book balance with the bank statement balance

- Drawn up by the bank to verify the cash book

- Sent by the bank to the customers when errors are made

- Sent by the bank customers to the friends.

- If two totals of trial balance do not agree, the difference must be entered in:

A real account B. The trading accounts C. A nominal account D. The capital account E. A suspense account

- The accounting equation is expressed in the financial statement called:

A. statement of financial position B. income statement C. expenditure statement D. reconciliation statement E. statement of change in equity

- If we take goods for own use, we should

- Debit drawings Account: Credit Purchase Account