CHAPTER 01 : SUBJECT MATTER OF ECONOMICS

By the end of this TOPIC you should be able to:

- Explain the meaning of basic economic terms including production, distribution, wants, economic resources, exchange and consumption and give the application of basic economic terms at family and community level.

- Define Economics according to different schools of thought; and justify the importance of studying Economics.

- Explain why Economics is both a science and an art subject; and describe the Normative and Positive Economics and its application in daily life.

- Differentiate between Micro- Economics and Macro- Economics and application in daily life.

- Explain the meaning of Economic Laws and give types and features of Economic Laws and describe main Economic problems and application in our daily lives,

- Explain the meaning of Capitalist, Command and Mixed Economy AND discuss features of Capitalist, Command and Mixed Economy and the merits and demerits of Capitalist, Command and Mixed Economy;

- Draw commerce chart and identify aids to trade components and differentiate Commerce from Economics

The subject matter of economics means what economics deals with. Economics as a subject deals with all the problems, which arise, in the following economic activities.

- Production.

- Consumption.

- Distribution.

- Exchange.

- Allocation of scarce economic resources.

- Human wants and their satisfaction.

Production

Production has two meanings.

(i) General meaning.

(ii) Economic meaning.

General meaning (General usage of the concept)

In this meaning production is a creation of goods and provision of services for personal consumption. For example, a carpenter who produces furniture for personal use but not for sale.

Economic meaning

In economic meaning, production is the creation of goods and provision of services for exchange in order to satisfy wants or is the creation of utility/satisfaction through exchange. For example a farmer who produces cash crops, private hospitals which provide medical services for sale.

Economics is concerned with problems which producers face in the process of producing due to scarcity of resources.

These problems are such as:

• What to produce.

• How to produce.

• How much to produce.

• For whom to produce.

• Where to produce.

• When to produce etc.

Economics enables producers to make choice of what to produce, how to produce, how much to produce etc with the scarce resources.

Consumption

Consumption is the process of making use of the commodity which has been produced. For example eating food, wearing clothes, driving a car, writing with a computer, reading an economics book or any other written material etc.

Consumption is actually the final stage of production. There would be no production if there was no consumption. Consumption enables production to continue. If goods produced by producers are not consumed, production will fail to continue.

Economics is concerned with solving problems, which affect the process of consumption due to scarcity of resources. Economics enables consumers to make choice of what goods or services to consume with their limited income.

Exchange

Exchange is the process of buying and selling goods and services. Production in economics is mainly for exchange. Economics is, therefore, concerned with all problems, which may arise in the process of exchange due to scarcity of resources.

Economics enables businessmen and women to decide which kind of goods or services to exchange in order to maximize profit. Also economics gives answers as to how much to exchange, when to buy or sell and for whom to sell in order to maximize profit.

Distribution

The word distribution has two meanings:

(i) General meaning.

(ii) Economic meaning.

General meaning (Meaning in general usage )

In this meaning, distribution means the process of transferring goods and services from areas of production to areas where they are needed for consumption. A good example is the distribution of Coca cola products which is done by the coca cola company by transferring their products from the factories to various shops throughout the country.

Economic Meaning

In economic meaning, distribution means the process of rewarding or making payments to factors of production from the total output produced or income generated in a firm or a nation. The reward is made to factors of production which are land, labour, capital and Entrepreneurship.

Distribution shows who gets what in the process of production, that is, how much wages the labour receives in the process of production, how much interest is paid to the owners of capital, how much rent is paid to owners of land and how much remains as profit to the entrepreneurs.

Economics gives answers to how much each factor of production should receive in the production process and the distribution of national income.

Human wants and their satisfaction Wants have two meanings:

General meaning (General usage)

In this meaning, wants refers to needs like food, shelter, clothes, T.V, Radio, etc.

Economic meaning

In economic meaning, wants are all human desires or things that must be satisfied by using certain needs. Examples of wants are such as hunger, thirst, education, and health. For example, one takes food to satisfy hunger and water to satisfy thirst. So in economic meaning food and water are not wants but means to satisfy hunger and thirst respectively.

Economics is concerned with satisfaction of human wants which are unlimited with the condition of scarce resources. That is, how can human beings satisfy their unlimited wants while resources are scarce?

Characteristics of human wants

Human wants have the following characteristics:

1. Human wants are unlimited in number.

2. All human wants cannot be satisfied because economic resources such as labour, capital and land which are used in the production process are scarce, that is, they are limited in number.

3. Wants can be satisfied by alternative means. For example, thirst for soft drinks can be satisfied by either some juice or soda.

4. Wants are felt again and again. When one want is satisfied, it tends to reoccur. For example, once thirst is satisfied, it tends to be felt again after some hours or minutes.

5. Wants are complementary. Some wants are satisfied by using two needs. For example, a want to drive is satisfied by a car and fuel.

Scarcity of Resources

Economics is concerned with scarcity of economic resources. Scarcity means limited in supply or less than what is required. In economic sense, all resources required to produce goods and to provide services are not enough to produce goods that can satisfy all human wants since are unlimited.

Scarcity is the main economic problem; there would be no economics if there was no scarcity. Economics is the subject that tries to solve the problem of scarcity of economic resources. It studies how human beings behave in meeting ends (wants) with the scarce resources.

Causes of Scarcity

Scarcity arises due to the following reasons:

(i) Limited stock of resources

(ii) Unlimited wants

(iii) Resources have alternatives uses

Limited stock of resources

Scarcity is caused by the fact that resources are limited in number (finite).Resources, in their particular sense, mean factors of production such as land, labour, capital and entrepreneurship. These resources are limited in supply; therefore, it is not possible to produce goods and services that can satisfy every human want.

Unlimited wants

Human wants are unlimited in number, therefore, the resources available cannot produce enough goods and services to satisfy all human wants.

Resources have alternative uses

Most of the resources have alternative uses. For example, land can be used to grow crops such as maize, rice, or as a site for construction of buildings. This means that if more land is used for farming, less land will be available for construction of buildings and other uses.

Solving the Problem of Scarcity

The problem of scarcity is solved differently in various economic systems.

1. Under Socialist Economy

In socialist economy the problem of scarcity is solved through economic planning in which the government allocates scarce resources, depending on the needs of the society. Since the aim is to promote the welfare of all the people, the government ensures equitable distribution of scarce resources. The government makes choices on behalf of the citizens and ensures that resources are used efficiently.

2. Under Capitalist Economic System

Scarce resources are allocated by the market forces of demand and supply. Scarce resources are used to produce goods and provide services that maximize profit or that are demanded by the consumers. Market forces decide what is to be produced, how to produce and for whom to produce. That is, market forces are responsible for making choices of what to produce and consume by using scarce resources.

3. Under Mixed Economic Systems

The decisions on how to use scarce resources are made by both the government through planning and by individuals through market mechanisms. The government allocates some scarce resources while the interplay of the market forces determines allocation of other resources.

Summary of the Subject Matter of Economics

In summary, Economics is a comprehensive subject; it covers broad aspects of production, consumption, exchange, distribution, human wants and their satisfaction, problem of scarcity of resources and choice.

Further to this, there is an economic element to any subject for instance, there is economics of education, social and welfare economics, transport economics, industrial economics etc.

Definition of Economics

There is no single definition of economics. In fact, there are as many definitions as there are the number of economists.

Reasons why there is no single definition of economics

The reasons why there is no single definition of economics are:

1. The subject matter of economics is very comprehensive (wide). Economics deals with many aspects. Therefore, one economist can define the subject basing on a certain aspect of the subject matter of economics. For example, basing on production, while another economist can define the subject basing on another aspect of the subject matter, like scarcity of economic resources.

2. The subject matter deals with human behaviour, which varies, from one person to another. People differ in tastes, in the way they see events etc. Economists are human beings, therefore they have room to differ. For example, should economic resources be allocated through the interplay of the market forces or through the government planning? The answers to this will depend on whether one is a socialist or a capitalist.

3. ''Economics is unfinished science'', With the passage of time, there have been significant developments in economic theory and new subjects have been included in it. Economics is still in the process of growth and development. In a science like economics, which is growing and developing, its correct and satisfactory definition, can be given only after it has sufficiently developed and grown.

Because of the above reasons various economists have given different definitions basing on the following:

- Definitions basing on wealth.

- Definitions basing on welfare.

- Definitions basing on scarcity.

Definitions basing on wealth

Adam Smith: He defines Economics as an inquiry into the nature and causes of wealth of nations.

John Stuart Mill: He defines Economics as the practical science of production and distribution of wealth.

Definition basing on welfare

Pigou: He defines Economics as the means of studying how total production could be increased so that the standard of living of the people might be improved.

Alfred Marshall: Hedefines Economics as a study of man’s actions in ordinary business of life. Economics inquires on how man gets his income and how he uses it. It is on one side the study of wealth and the study of man, on the other.

Definition Basing on Scarcity

A definition by Lord Robbins - According to Lord Robbins, Economics is a science which studies human behaviour as a relationship between wants and scarce means which have alternative uses. Thus economics is a study of a particular kind of economizing.

Characteristics of Robbins’ Definition

Robbins definition has the following characteristics:

(i) Wants are unlimited.

(ii) Resources have alternative uses.

(iii) Resources are scarce.

(iv) Economic problems arise due to scarcity of economic resources.

Strengths of Robbins’ definition

Robbins' definition has the following strengths:

(i) The strength of Robbins definition is that it is centered on Scarcity that is the main economic problem. This is a fact, since if resources were not scarce, economics would not exist and there would be no need to economize, to him every human activity has an economic aspect on it as long as there is scarcity while other definitions do not consider the problem of scarcity.

(ii) Robbins’ definition is applicable to all economies and covers both macro and micro - Economics while some definitions base on either microeconomics or macroeconomics for example Alfred Marshalldefined economics as a study of man’s actions in ordinary business of life. It inquires how he gets his income and how he uses it. It is on one side a study of wealth and on the other side the study of man; this definition is based on microeconomics analysis.

(iii) Robbins’s definition does not distinguish between material and non-material activities. According to him, there is economics to every human aspect as long as there is scarcity. This is unlike other definitions, like that of ADAM SMITH who defines Economics as a study of the ‘’nature and causes of wealth of nations’’, this definition considers wealth as an end in itself and does not consider welfare commodities.

Limitations of Robbins’ definition

Although Robbins’ definition is better than other definitions it has the following weaknesses:

(i) It looks at Economics as a science of individual behaviour and not as a social science. Many economists are of the view that economics is a social science and it should study the problem of choice when it has a social aspect that is when a man’s choice affects other members of the society. Thus according to Scitorsky ‘’economics is a social science studying how people attempt to accommodate scarcity to their wants and how these attempts interact through exchange’’. It is, thus clear that contrary to the views of Robbins, economics has been regarded by many economists as a social science, since a choice made by an individual must have effects to the other members of the society.

(ii) It gives little emphasis on other subject matters of Economics such as production, exchange, consumption and distribution.

(iii) It says nothing about economic welfare.

(iv) According to him Economics should study only the allocation of scarce resources in the production of various goods and services hence how the prices of goods, services and resources are determined, but the scope of economics is wider than the allocation of resources and the price theory. These days the importance of macroeconomics has increased in such that we study how the national income of a country change.

(v) Robbins's definition is also criticized on the ground that it does not cover the theory of economic growth and development. The theory of economic growth and development studies how the national income grows over a period of time, and what factors cause such increase. With economic growth the productive capacity of the country expands and brings about an increase in national income and the level of employment.

While Robbins's takes the resources as given and talks about their allocation, the theory of economic growth is concerned with reducing the scarcity of resources through raising the level of national income and accumulating more capital and wealth. For example in developing countries the question of economic growth is more important because these countries are making efforts to remove poverty of their people and to raise their living standards through economic growth. In recent years many theories regarding how to initiate and accelerate economic growth in developing countries have been propounded.

The theory of economic growth has now become the core of the science of economics both in developed and developing countries and thus Robbins definition is defective because it does not cover an important subject like economic growth.

(vi) Even the problem of unemployment which is being faced by both developing and developed countries of the world, is not covered by Robbins definition. The definition deals with the problem of scarcity, however the problem of unemployment is not the problem of scarcity but due to abundance of manpower in relation to the demand for it. Labour is an important factor of production and its unemployment implies that it is abundant and not scarce.

Some recent definitions of economics

1. Professor Henry Smith definition

“Economics is the study of how in a civilized society one obtains the share of what other people have produced and of how the total product of a society changes and is determined. By civilized society it is means that there are some legal institutions as well as rights of property and other things in the society’’.

2. Jacob Viner.

‘’Economics is what economists do’ According to Jacob viner in other words what economics is about can be better understood from what economists do and what they have been doing. That is to say what type of questions economists ask and provide for them. Thus what economics is about or in other words what is the subject matter of economics can better be known by spelling out the questions economists ask and have been asking.

Why do economists disagree with each other or why do Economists agree to disagree?

Reasons 1. Deficiency of statistical data

Statistical information on economic affairs may have some deficiencies which leave room for disagreements amongst economists. For example, one can say Tanzania must remain in the East Africa Cooperation since it leads to faster economic growth. Economists may differ because they may not be sure whether economic development has accelerated since Tanzania joined the East Africa cooperation. These doubts arise due to the fact that national income statistics have a number of deficiencies. For example over-estimation of non-commercial sectors and exaggeration of figures due to inflation.

2. Economics is a young science

Although the subject of economics is as old as the human race, economics as a scholarly discipline is very young. There are many theories and models which have been developed but some have not been fully tested, either because of insufficient time that has elapsed to provide adequate data or because no one has found a satisfactory way of testing them. Lack of reliable data provides room for economists to differ.

3. Techniques and economic changes

These bring about changes in economic behaviour so that assumption about human behaviour which serves as useful basis for formulation of economic theory at one period of time may change due to technological changes. For example Malthusian theory of population later was proved to be wrong due to technological innovations in agriculture which took place in 20th century hence enabled nations to increase food production and feed the large population.

4. Economics is a wide subject

The fact that there are many definitions of economics means that the subject matter of economics is very wide and a group of economists could each approach the subject from a different aspect of the subject matter and they are bound to differ.

5. Economics is dealing with human behaviour

Economics deals with human behaviour which is varied in nature. People differ in tastes and the way they see events. Economists are human beings therefore they have the room to differ in the way they make value judgment. For example whether economic resources should be allocated through the interplay of the market forces or not. The answers to this will depend on whether one is a socialist or capitalist.

6. Relationship between Economics and other subjects

The study of economics is related to the other disciplines like natural sciences, political science, geography and history, because of the relationship between economics of a place or a country and various scientific, geographical, political or historical aspects of a particular place or country. For example, whenever there are technological developments in any place it would have impact on the economic activities or wherever there is political stability in a place, economic prosperity will follow etc.

7 . Economics as a science

A science is a systematic body of knowledge concerning the relationship between cause and effects of a particular phenomenon. Science is a sum of those facts which are found to be correct after experience and experiments. Economics is regarded as a science because of the following factors:

(i) It is a systematic study. As a systematic studies, it involves data collection, analysis, experiments and making conclusion.

(ii) Economics has laws and theories. As a science economics has laws made on the basis of cause and effect relationship. Economic laws are statements of scientific truth regarding the allocation of scarce resources. Examples of economic laws are laws of demand and supply, law of diminishing returns etc.

(iii) Economics has scales and measurements, as in science, in economics, money is used as a scale of measurement of the value of goods produced.

(iv) Economics uses experiments although Economists do not have laboratories like natural scientists, they are able to evaluate the cause and effect of economic events on the basis of experiences of human behaviour.

(v) Economists predict events, like in natural sciences. Economists can predict events. For example economists can predict the effects of unfavorable weather on the supply of agricultural products in predictions economists apply economic laws.

However economics is not a pure science, therefore it differs from natural sciences in the following ways:

• There are no laws which can explain human behavior because people are unique and it is not easy to predict human behavior.

• Money is not a free measure of economic events because its value tends to change.

• Economic laws are based on assumptions, therefore, they are subject to limitations.

Economics as a Social Science

Economics is regarded as a social science because its principles and laws relates to the behaviour of people. It regards human behaviour as a relationship between scarce resources and wants. Like other sciences it is simply a study of causes and effect, although economists cannot carry out laboratory experiments they do observe and collect data from which they derive principles or laws concerning the economic behaviour of people.

Economic as an Art

As an art, it involves the utilization of scientific facts of science for practical purposes.

Economics and Political Economy

Economics is a branch of social science, which is concerned with the use, and allocation of scarce resources for the maintenance of growth and stability; it studies how people in society choose to allocate scarce resources for the betterment of the society. Political economy is the branch of social science, which deals with the study of development of social production, i.e. economic relations among the people; it deals with laws governing production, distribution, exchange and consumption of the material wealth of human society at various stages of development.

Approaches to Economics

There are two approaches to economics these are:

(i) Positive economics

(ii) Normative economics

Positive economics

Positive economics deals with description and analysis of the existing economic situation, it explains how an economic unit or an economic system works and operates under given conditions. Positive economics answers questions such as what determines the level of employment. How will a particular fiscal or monetary policy affect investment, consumption etc positive economics points out the causes of economic problems.

Normative economics

It involves value judgment. Economists under normative economics advise how the economy should operate, it suggests aims and objectives for the economy and points out what ought to be done to achieve them by suggesting what should be done to remove economic problems.

Differences between positive economics and normative Economics

(i) Positive economics merely explains economic phenomena i.e. why things are as they are while normative economics considers what ought to be done to solve a certain problem, example what should be done to remove income inequality.

(ii) Positive economics is concerned with the utilization of means or resources for the achievement of certain economic goals while normative economics discusses the desirability of the ends or goals to be achieved.

(iii) Positive economics is not worried of the ends of any decision whether bad or good while normative economics concerns itself with the goodness or badness of the economic ends.

Usefulness of Studying Economics

The knowledge of economics is helpful in the following ways:

Resource allocation

The knowledge of economics enables the owners of resources/ producers to make choice of what and how to produce with scarce resources.

Price determination

The knowledge of economics enables producers/firms to set a level of price, which maximizes profit given existing demand conditions.

Costs minimization

The knowledge of economics enables producers to choose the least cost combination of factors.

Formulation of development policies

The knowledge of economics helps the government to formulate development policies. For example, a policy to stabilize the economy and promote industrialization.

Utility maximization

Consumers by using the knowledge of economics are able to make choices that can maximize satisfaction i.e. efficient utilization of resources.

Branches of economics

The subject matter of economics can well be subdivided into Microeconomics and Macroeconomics.

Macroeconomics

It is the branch of Economics which studies aggregate economic variables, these are, variables which tend to affect the economy as a whole. For example, the study about national output, money supply, government spending, the levels of taxes, inflation, unemployment etc.

The subject matter which fall under Macroeconomics are:-

(i) Theory of national income and employment.

(ii) Theory of general price level and inflation.

(iii) Theory of economic growth.

Importance of macro-economics

Macroeconomics has the following importance:

1. It explains what determine the level of national income and employment and what causes fluctuations in the level of national income output and employment. It explains the growth of national income over a long period of time. In other words macroeconomics examines the determination of the level, fluctuations and trends in the overall economic activity.

2. It is helpful in giving macro-decision. For Example, about the total amount of money supply, government expenditures, level of taxation, and new investment during a particular year.

3. Macro-economics is very important in formulation of policies and plans which can be used to solve various economic problems. For example monetary and fiscal policies are macro-economic policies which are used to stabilize the economy and solve economic instabilities such as inflation.

4. Macro-economics is a very useful instrument for the government to deliberately control, influence and direct economic activities and variables in a country. For example reduction of taxes which is a macro-economics decision can have effect on the growth of investments in a country.

Limitations of macro-economics

Macro economics has the following limitations:

1. Macroeconomics cannot analyze the objectives and decisions of individual economic units. For example, how firms or consumers should make choices on what goods to produce or to consume or of how much should a government spend on a specific project.

2. Macroeconomics decisions have little effect on the activities of individual units. For example a decision to reduce taxes in order to stimulate aggregate investment will have little impact on the production of individual fishermen if these taxes are not imposed on the inputs used by the fishermen.

3. It is very difficult to apply “ceteris paribus” rule under macro-economics since one macro economic variable can affect other macro-economic variables unlike microeconomics variables. For example, when there is hyperinflation all the economic variables, such as employment, income and investment will be affected

4. Problems which affect individual firms and consumers cannot be well solved by macro-economic decisions. For example when a firm is faced with a problem of capital it cannot directly benefit from the instruction of the central bank to reduce interest rate if the firm does not have securities for securing loans.

5. Macroeconomics ignores individual differences among economic units and thus cannot effectively solve specific problems which affect these units. For example a macro – economic policy of liberalizing marketing of agricultural output in a country may benefit a group of peasants who are facing a problem of market for their product but the policy would be meaningless to another group of peasants in another area who do not face the problem of market for their products but are facing a problem of declining output due to severe drought and lack of farm implements.

Microeconomics

Micro economics is a branch of economics, which studies individual parts of the economy. (Micros is the Greek word for small).

The subject matters of microeconomics include:

(i) Determination of relative price levels of commodities and resources.

(ii) Distribution of factor incomes.

(iii) Economic and welfare efficiency.

Importance of micro-economics

Microeconomics has the following importance:

1. It analyses the objectives and decisions of individual economic units, that is, individual consumers, firms, government agencies or specific projects. For example, how a consumer should make a choice of about what goods and services to buy or a choice of what goods to be produced by a firm, or a government agency decision about how much to spend on a specific project.

2. Microeconomics decisions affect macroeconomics variables. For example, consumers’ choice on goods and services has effect on aggregate consumption.

-Also a firm’s decisions on what to produce have effect on aggregate investments.

Likewise government decisions on levels of taxes must have considerations of individual consumer’s reactions on rise or decline in levels of prices.

3. Price determination is based on micro-economics; producers/firms will set prices depending on responses by individual consumers in the market.

4. Problems which affect individual firms can well be solved through a microeconomics study. Micro-economics enables decision makers to decide on what goods or services should individual firms produce with scarce resources.

5. It explains the conditions of efficiency in consumption and production and highlights the factors which are responsible for the departure from the efficiency or economic optimum. On the basis of this, microeconomics theory suggests suitable policies to promote economic efficiency and welfare of people.

Therefore not only does microeconomics theory describes the actual operation of the economy, but it has also a normative role in that it suggests policies to eradicate inefficiency from economic systems so as to maximize satisfaction or the welfare of the people.

6. Microeconomics explains how a free market economy, with its millions of consumers and producers work to decide about the allocation of productive resources among the thousands of goods and services.

7. Microeconomics addresses a big question about who gets what out of the output produced.

8. Microeconomics analysis is also usefully applied to the various branches of economics such as public finance and international economics. In public finance, it is macroeconomics analysis which is applied to explain the factors which determine the distribution of incidence or the burden of a commodity tax between producers or sellers on the one hand and consumers on the other. Further, microeconomics analysis is applied to show the damage done to social welfare or economic efficiency by the imposition of tax.

If it is assumed that resources are optimally allocated or maximum social welfare prevails before the imposition of tax, it can be demonstrated by microeconomics analysis what amount of damage will be caused to the social welfare. In international economics microeconomics show whether devaluation will succeed in correcting the disequilibrium in the balance of payment depending on the elasticity of demand for exports and imports.

Limitations of micro-economics

Microeconomics has the following limitations:

1. Micro-economics study does not give explanation on how aggregate variables perform. For example, how the gross national product grows over years.

2. Micro-economics cannot create policies to solve problems which affect the whole economy, and problems which affect the whole system. Examples of problems which can not be solved effectively by applying microeconomics policies are inflation, unemployment, deflation etc.

3. Micro-economics is weak in effecting national development plans and policies.

4. Micro economics works under ceteris paribus conditions which may not be realistic due to changes in economic conditions.

Interdependence between macroeconomics and Microeconomics

Theories regarding the behaviour of some macroeconomics aggregates are derived from theories of individual behaviour. For example, the theory of aggregate demand which comprises of aggregate consumption and aggregate investment are derived from the behaviour of individual consumers and individual investors respectively.

Microeconomics theory contributes to macroeconomics theory in another way. For example the theory of relative prices of products and theory of relative prices of product is essential in the explanation for determination of general price level. Even Keynes used microeconomics theory to explain rise in general price level as a result of the increase in money supply. According to Keynes, when as a result of the increase in money supply, aggregate demand in an economy increases and more output is produced, the cost of production rises. With the rise in the cost of production, the general price level rises. There are several interdependencies among macroeconomics and microeconomics variables. For example, the determination of rate of profit and interest greatly depend upon the macroeconomic aggregates. In macroeconomics theory profits are regarded as reward for uncertainty bearing, but microeconomics theory fails to show the economic forces which determine the magnitude of profits earned by the entrepreneurs and why there are fluctuations in them.

It is, therefore, true that profits of individual firms depend upon the level of aggregate demand, national income and the general price level. For example at times of depression, when the level of aggregate demand, national income, general price level are low, entrepreneurs get losses. On the other hand, when aggregate demand, incomes of the people, general price level go up and conditions of boom prevail, entrepreneurs earn huge profits.

Differences between macro- economics and micro-economics The main differences between microeconomics and economics are:

(i) Macroeconomics is a branch of Economics, which deals with economic variables which affect the whole economy. Examples of such variables are national income, unemployment, inflation etc. On the other hand Microeconomics is a branch of economics which deals with individual units of the economy such as firm’s output, production and pricing of individual commodities, wages of individuals etc.For example a study about the level of output and employment in the Tanzania’s textile industry belongs to microeconomics while a study about the output and employment in all economic sectors of the country belongs to macro economics.

(ii) Macroeconomics deals with aggregates of the economy such as total consumption, national output, and inflation etc. while microeconomics deals with individual firms or consumers such as output, cost, pricing of commodities of individual firms and wages and consumption of individual consumers.

(iii) Macro economics gives explanation of the performance of aggregates variables of the economy such as the growth of national income while microeconomics gives explanation of performance of a single firm or consumer.

(iv) Microeconomics policies are more effective in solving problems, which affect individual firms while macro economics is applied only to problems which affect the whole economy such as inflation, slow economic growth and unemployment and therefore less effective in solving individual problems.

(v) Microeconomics is effective in development of individual firms while macroeconomics is more effective in development of all economic variables in a nation.

(vi) Microeconomics works under ceteris paribus condition since changes in one firm cannot have significant impact on other firms while macroeconomic changes have widespread effects, therefore cannot work under ceteris paribus condition. For example when a single firm’s output increases it will cause little changes on other firms’ output and on aggregate variables in the economy such as employment, inflation and consumption but when one macroeconomic variable changes it will cause changes in other economic variables. For example when national income increases it cause changes in other macro economic variables such as consumption, employment and investments therefore macroeconomics can not work under ceteris paribus condition.

The main economic problem

The main economic problem is to make choices on what, how, and for whom to produce under the situation of scarce resources, alternative uses of resources and unlimited human wants.

How the economic problem arises?

Economic problem arises because individuals’ wants are virtually unlimited, whilst the resources available to satisfy those wants are scarce.

Fundamental questions of economics

Every society/firms is faced with several questions due to scarcity of resources:

What should be produced?

Every society/firm must decide on what goods and services are to produced. Since resources are scarce no economy or firm can produce enough goods or services demanded by the consumers.

Producing more of one commodity will often mean sacrificing production of another commodity; this means that the society as a whole or individual producers must make a choice of what goods to be produced with the scarce resources

How should this product be produced?

Once what sholud be produced has been decided and the quantity has been determined, decisions on how should it be produced must be made. There are many types of factors of production or inputs into the production process. Usually a business firm can use many different combinations of factors of production to produce its product. Each firm must decide on the particular combination of inputs to be produced, in this case a firm will choose a least cost combination of inputs, which minimizes costs.

Who gets what?

These are the returns to factors of production, like , wages for labor, interest for capital, rent for land and profit for entrepreneurship. Distribution is fundamental because it can cause social and political unrest; therefore at the end of production process return for each participant in the process of production must be established. “Because how a cake is prepared may not be important but how the cake is distributed is very important”.

For whom should the output to be produced?

Producers must ask themselves, who will be their potential customers for their products; this is important because production in economics is for exchange, therefore the question is who will be the potential buyers?

When to produce?

This is a decision on whether to produce now or to produce in future.

Where to produce?

This is the decision on location of the firm whether to locate the firm near the source of raw material or near the market.

Answers to economic questions under different economic systems :

Capitalist/Free enterprise economy

Under this type of economic system, price mechanism gives answers to all economic problems/questions.

What is to be produced should be those commodities that consumers are willing and able to buy at the current market price ie price which generates enough revenue to cover the costs of production. However it should be understood that price mechanism is not a panacea to all economic questions or problems.

In socialist/command economy

In a command economy, all fundamental questions of what should be produced, how to produce are decided by the government through a central planning organ which determines on behalf of the society what kind of goods or services to be produced.

In mixed economic system

In mixed economic system, economic questions are answered by both the market mechanisms and by the government through economic planning. In mixed economic system, some goods are produced depending on the demand and supply conditions while other goods are produced according to the plans made by the government.

Scarcity, choice and opportunity cost

(i) Scarcity

In economics, the term scarcity simply means limited in supply or less than the requirement. In economic sense, all things are scarce as relative to the people’s desire for them.

It is a fact that human wants are unlimited but the resources needed to produce goods which can satisfy wants are limited in supply. It is therefore impossible to satisfy all wants of every human being. Scarcity is caused by the following factors:- - Limited stock of economic resources.

- Unlimited human wants.

- Resources have alternative uses.

Since scarcity is the main economic problem or the central problem of economics, there is no economics if there were no scarcity, because economics is all about economizing of economic resources. If resources were not scarce there would be no economic problems and consequently no economics.

(ii) Choice

Since resources are scarce, a selection or choice of few alternatives to be satisfied must be made. Producers must choose what goods or services to produce or how to produce given scarce resources. Consumers too must decide which of their wants must be satisfied by using their limited incomes. Economics is therefore about scarcity and choice.

(iii) Scale of Preference

A scale of preference is a list of wants in the order of their importance starting with the most pressing wants ending with the least pressing wants. The most pressing wants should be the first to be satisfied followed by the least pressing wants, some wants will be left unsatisfied due to scarcity of resources, the unsatisfied wants are the real cost or the opportunity cost of the wants satisfied, a scale of preference is usually made by producers or consumers in order to maximize utility in a situation of scarce resources and unlimited wants.

(iv) Opportunity Cost

The opportunity cost of anything is the alternative that has been foregone after making a certain choice due to scarcity of resources. Since people cannot satisfy all their wants due to scarcity of resources they must therefore choose between one thing and another thing so that the satisfaction of one want involves sacrificing another want. Likewise since the supply of factors of production is limited, the production of one thing often involves a sacrifice of production for another commodity.

Examples of opportunity cost:

Example I:

If a student has two alternatives of using his/her evening time, to do homework and another alternative is to play football. If he/she chooses to play football then the opportunity cost of playing football is the homework foregone.

Example II:

If a farmer has two alternatives of using his/her field, one is to grow maize and the other one to construct a building for keeping cattle. If he chooses to cultivate maize there will be no land or site for construction of a building for his cattle. The opportunity cost of growing maize will be the building for the cattle sacrificed.

Illustration of opportunity cost by using production possibility curves

Production Possibility Curve (PPC)

This is a locus of points showing combinations of commodities that may be produced when all resources are fully utilized. With limited resources an economy has limited possibilities for production of goods and services. Increasing production of one often leads to less production of another type of goods. For example, as the government increases military expenditure the provision of social services declines or deteriorates.

This can be illustrated by using a production possibility curve or frontier. For example in the production possibilities for Rungwe District, we assume a simple hypothetical case, in which the district has limited land resource and therefore can produce only two crops, coffee and banana, we also assume that all resources are fully and efficiently utilized, and that land is fixed in supply. Thus, when farmers increase the production of coffee it means less production of bananas and when peasants increase production of bananas it means less production of coffee.

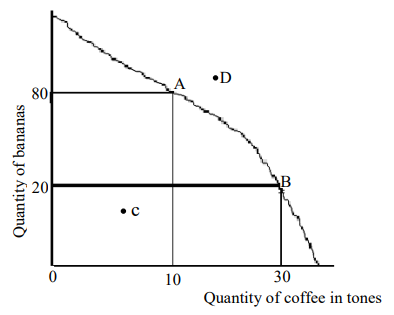

Quantity of coffee in tones Figure: 1.1 Production possibility curve |

In figure 1.1,

- The quantity of coffee in tons produced is measured along the horizontal axis and the quantity of banana in tons is measured along the vertical axis.

- Point A and B show attainable combinations and feasible combinations when resources are fully utilized. At point A the district can produce 80 tons of bananas per year when it produces 10 tons of coffee. At point B the district can produce 20 tons of banana and 30 tons of coffee. Points A and B are alternatives choices for the district.

- Point D shows unattainable combinations because the resources are not enough to produce such a quantity. In other words point D is not feasible and shows scarcity of resources.

- Point C represents either inefficient use of the district’s resources or underutilization of resources.

The opportunity cost of either product is represented by negative slope of the boundary. Opportunity cost can be calculated as;

Fall in bananasproduction Risein coffee production

|

Table 1.1. Output of two commodities under production possibility

| Product combination | Tons of coffee | Tons of bananas | Opportunity cost of one ton of coffee |

| A | 10 | 80 | 3 units of bananas |

| | | | |

| B | 30 | 20 | |

Table 1:1 above, shows the opportunity cost of Coffee in terms of number of tons of banana which must be foregone to obtain a one unit increase in tons of coffee. An increase by 20 tons of coffee from 10 units to 30 units results into the decrease by 60 units of banana from 80 units to 20 units hence 3 units of banana decrease per one unit increase in tons of coffee OR 3 units of banana increase per one unit decrease in the production of coffee that is, the opportunity cost of one unit of coffee is three units of banana.

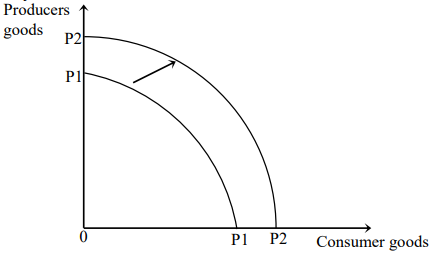

Shift of the Production Possibility Curve

A PPC can shift rightwards due to the following factors:

(i) Improvement in technology.

(ii) Economic growth.

(iii) Increase in productive resources namely capital, land and labour.

Diagrammatically it can be shown as follows.

Figure: 1.2 Shift of a production possibility curve |

In figure 1.2, a change in any of the factors above let say increase in capital will shift the curve from P1P1 to P2P2.

Uses of production possibility curve

The knowledge of production possibility curve is useful in the following ways:

1. Allocation of scarce resources PPC enables the society to make a good decision on how to use scarce resources to produce goods that maximizes social welfare. With limited resources a society has to make a choice of the combination of goods within the production possibility curve.

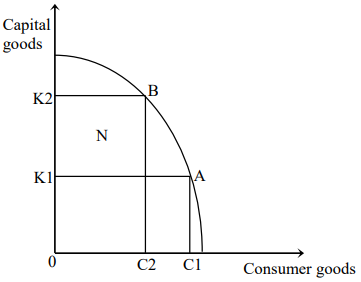

2. To indicate problem of unemployment and underemployment of resources. When the economy is operating at a point below the production possibility curve it implies underemployment of resources.

Figure: 1.3 Point N shows underemployment of resources |

3. To show full employment of resources. When the economy is operating at any point along the PPC it shows full employment of resources as it can be shown in figure 1.4 below.

Figure: 1.4 PPC showing full utilization of resource |

In figure 1.4 above, point A and B show full utilization of resources.

4. To increase capital formation and economic growth.

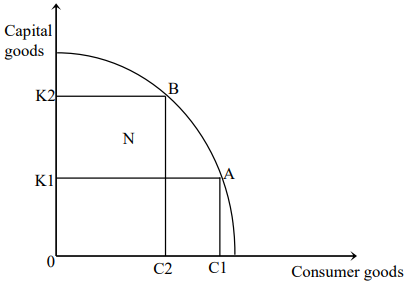

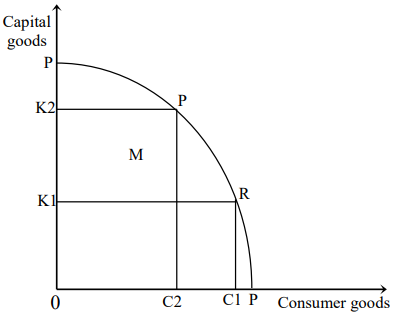

Another important use of the production possibility curve is that, with it we can explain the problem of capital formation and economic growth. With limited resources a society has to decide on the amount of capital and consumer goods to be produced. When the society allocates more resources for the production of consumer goods, fewer resources will remain for the production of capital goods. In order to increase production of capital good the society will have to withdraw some resources from the production of consumer goods and use them for the production of capital goods. This is shown in figure 1.5 below.

Figure: 1.5 Production possibility curve |

In figure 1.5 above, the economy has allocated the available resources between capital and consumer goods in such a way that when it operates at point R on the production possibility curve PP it produces OC1 of consumer goods and OK1 of capital goods. Now suppose that the society decides to produce more of capital goods. To implement this decision the society will have to withdraw some resources from the production of consumer goods to the production of capital goods. As a result the production of consumer goods will decline. The reallocation of consumer goods and capital goods will cause a movement in PPC from point R to point P. The society will now produce OK2 of capital goods and OC2 of consumer goods.

Importance of the Concept of Opportunity Cost

The concept of opportunity cost is very important in any economic decision involving scarce resources. Since resources are scarce relative to the people’s desire for them, satisfaction of one want involves sacrificing another want. This means that certain wants are satisfied at the expense of other wants.

What wants to be satisfied and what wants to be foregone will largely depend on the opportunity cost of a want to be satisfied. A rational consumer or producer will choose a want which has a low opportunity cost, the opportunity cost can be measured in terms of marginal utility of the consumers or returns in terms of output to producers. For example, if marginal utility obtained by a student by using his evening time for studies is higher than by going to the movie then this particular student will choose studying because studying has low opportunity cost in terms of marginal utility.

Likewise a peasant will choose to grow rice in his/her land if the land produces more units of rice than other crops, assuming the price per unit of output and the cost of employing resources for all crops is the same.

The government planners also apply the concept of opportunity cost in the process of planning. For example, if increasing expenditure on purchasing military hardware it implies deterioration of the standard of education, poor health services, poor road, malnutrition and social unrest, then planners should reduce expenditure on military hardware because such expenditures have very high opportunity cost.

Entrepreneurs also apply the concept of opportunity cost in order to retain workers. Workers will normally like to supply their labour to firms where the transfer earnings or the opportunity cost is low. For example, if a worker in firm A is paid 100$ per month and in firm B he would be paid 50$ per month, this particular worker will continue to work in firm A because the opportunity cost of working in firm A is lower than that of working in firm B.

In this case the employer of this particular worker in firm A will continue to pay the worker amount above 50$ per month in order to retain him in his firm.

However the assumption here is that always labour or any factor of production has alternative use or is perfectly mobile. In international trade the concept of opportunity cost is a basis of the theory of comparative cost where relative costs are important in determining which products are imported and exported. A country will export a product for which it has relatively low opportunity costs and will import a product for which it has relatively high opportunity costs in production as shown in the example below.

Table 1. 2 Labour units required to produce output in Kenya and Tanzania.

| Country | Units of labour required to produce | |

| 1 barrel of maize | I bolt of cloth | |

| Kenya | 90 | 60 |

| Tanzania | 30 | 30 |

In table 1.2 above, Tanzania has absolute advantage in the production of both commodities since it takes fewer units of labour to produce both products than it does in Kenya. But by looking into internal cost ratios of each country, Tanzania has absolute advantage in both maize and cloth; however its absolute advantage is greater in maize (90/30 > 60/30). It can out produce Kenyans by 3 to 1 in maize but only 2 to 1 in cloth. A greater absolute advantage, such as Tanzania has in maize is called comparative advantage, compared to Tanzania , Kenya is at absolute disadvantage in both maize and cloth, but it is at a lesser absolute disadvantage in cloth (60/30 < 90/30), where the Tanzanians out produce it only by 2 to1. A lesser absolute disadvantage is also called a comparative advantage. Thus Kenya has a comparative advantage in cloth production and can gain from trading its cloth for Tanzania’s maize.

Other Main Economic Concepts Goods

Goods are things which can satisfy human wants like cloths, cars, horse, radio, T.V etc.

Classification of Goods

Free goods Vs economic goods Free goods

These are the goods which are provided freely by nature for example air, sunshine, rainfall, ocean water, forest etc.

Features of free goods

- They are not scarce, that is, they are abundant.

- They are not produced through human effort.

- They are not transferable in terms of ownership.

- They lack exchange value.

- They possess utility (use value).

Economic goods

These are the goods that are produced by human effort and possess the following qualities.

- They have utility (Ability to satisfy wants).

- They have exchange value that is they can be bought and sold.

- They are transferable in terms of ownership from one person to another person.

- They are scarce.

| Note: Economics is concerned with Economic goods not Free goods because production in economics is for exchange and economic goods have exchange value. |

Consumer Goods Vs Producer GoodsConsumer goods

These are the goods produced for final consumption such as food, radio. T.V, furniture etc.

Producer goods: Are those goods, which are produced to assist production of other goods. They are also known as capital goods. Examples of producer goods are machinery, raw-materials, workshops, buildings, roads and railways.

Perishable Vs Durable GoodsPerishable goods

These are the goods, which can easily be destroyed or decayed. Examples of perishable goods are foodstuffs, like milk, meat, floor, fruits, vegetables, etc.

Durable goods

These are the goods, which can stay for a very long period of time without being destroyed. Examples of durable goods are buildings, machinery, furniture etc.

Private Vs Public Goods Private goods

These are goods owned exclusively by individuals. For example private cars, TVs, clothes, houses .etc.

Public goods

These are the goods owned and enjoyed collectively. For example, defense, roads etc.

Features of public goods

Non - divisibility

Public goods are provided in totality to the public. For example defense is provided in totality to all the citizens.

Non-rivalry

There is no competition in consumption, one person can consume extra units without reducing consumption of other consumers.

Non-excludability

No one is excluded in consuming public goods; public goods are consumed by all people.

Free rider problem in consuming public goods

This problem exists because there are some individuals who want to enjoy public goods without paying for them.

Intermediate goods vs. final goods

Intermediate goods are the goods in progress of production while final goods are goods ready for consumption

Normal Goods Vs Inferior Goods

Normal goods are the goods whose demand for which their demands increase when real income increases and their demand decreases when income of the consumer decreases. While inferior goods are the goods whose demand of consumers decrease when real income increases.

Wealth

Wealth is any stock of goods existing at a certain time that conforms to the following requirements:

(i) They must posses utility, that is, they must yield satisfaction.

(ii) They must have a money value. (iii) They must be limited in supply.

(iv) It must be possible to transfer their ownership from one person to another.

Types of Wealth

Personal wealth

These are the personal belongings of individuals such as house, radio, furniture etc

Business wealth

This is the wealth, which is used in business. Examples of business wealth are machinery, factory building, etc.

Social wealth

These are the types of wealth, which are communally owned. Examples of social wealth are schools, hospitals, roads etc.

Utility

This is the satisfaction obtained by people in consuming goods or services. Different consumers of goods or services may get different utilities from the same commodity at different times and situation. In this sense, it is very difficult to measure utility that a person gets from consuming goods and services.

Usually, the demand for a commodity is largely influenced by marginal utility, that is, the additional satisfaction that a person obtains from consuming a commodity influences the person to buy more or less.

Diminishing Marginal Utility (Law)

Marginal utility is the additional satisfaction that a person obtains after consuming additional units of a commodity. The law of diminishing marginal utility states that the more of a thing a person possesses the less satisfaction he will derive from it. That is, each successive increment in consumption of units of a commodity yields less satisfaction than the previous unit until eventually satiety is reached. For example, the utility that is derived from drinking water diminishes as a person drinks more glasses of water.

Forms /Types of Utility

There are three forms of utility:

Place utility

This refers to the process of transferring a commodity from where it is produced to where it is needed for consumption. This leads to increased production since it enables products to reach the market and therefore increases the consumption of the goods as consumption increases firms are able to carry on further production.

Form utility

This is a utility obtained when a commodity is changed in terms of its form from a less useful form to a more useful form. For example processing raw materials to finished goods. Form utility leads to increased value and demand for a commodity. Due to increased value and that lead to increase in demand, firms are encouraged to increase production.

Time utility :

This is a utility obtained when a stored commodity is made available at a time when it is needed for consumption. Time utility ensures constant supply of a commodity and thus reduces fluctuations in the demand for the commodity.

Economic Laws

- These are statements, which show the relationship between economic variables.

Economic laws show what happens under a given economic conditions.

- Economic laws regulate relationships in main economic activities of production, exchange, consumption and distribution.

- Economic laws assist in various economic decisions like allocation of scarce resources, determination of prices, choice of methods of production etc.

Examples of economic laws are laws of demand and supply. These laws state as follows:

The law of demand

Other things remain constant the lower the price of the commodity the higher the quantity of the commodity that will be demanded.

The law of supply

This law states that the higher the price of the commodity the more the quantity of the commodity will be supplied, assuming ceteris paribus. Therefore, economic laws show tendencies of what happens under given economic conditions. They express people’s reactions to economic forces. For instance in the above examples, the law of demand shows that, consumers tend to buy more as the price of the commodity decreases and suppliers tend to supply more when the price of a commodity increases. However, sometimes people behave contrary to the laws. For example, under conditions of exceptional demand people with low incomes buy more inferior goods at a higher price than at a lower price.

Characteristics of Economic Laws

Economic laws have the following characteristics:

(i) They are not static i.e. they change with change in time and economic conditions.

(ii) They are hypothetical and conditional. Unlike the laws of physical sciences which are quite exact, precise and definite and therefore can predict the coarse of events, economic laws lack this predictive value. Laws of economics are conditional and are associated with number of qualifications and assumptions. These assumptions are generally contained in a phrase other things remaining the same. For example according to the law of demand, when the price of a commodity rises, its quantity demanded by the consumers will fall, assuming that other factors such as income remain the same.

Classification of Economic Laws

Economic laws can be classified under the following categories:

(i) Pure and natural economic laws

(ii) Laws of the super structure (Government or state law)

(iii) Specific economic laws

(iv) General economic laws

(i) Pure and natural economic laws

These emerge purely from interactions of economic variables such as price and quantity demanded or supply, scarcity, choice etc. These laws have a characteristic that they can operate in all economic systems; Examples of pure economic laws are the law of demand and supply and the laws of diminishing marginal utility.

(ii) Laws of the super structure (Government or state law)

These are laws made by the government or state to regulate or control economic activities. Examples of laws of the superstructure are:

- Laws of taxation.

- Laws of controlling consumption of certain commodities.

- Laws of stabilizing the economy.

- Commercial laws.

(iii) Specific economic laws

These are the laws which are specific to a certain economic system. These laws control the relationship of people in the process of production, consumption, distribution and exchange. Once a system is replaced by a new system, specific laws are replaced by the laws of the new system. Examples of specific economic laws are:-

- Law of private ownership of major means of production under capitalist system.

- Law of public ownership of major means of production, this law operates under socialist system.

(iv) General economic laws

These are laws which operate in all economic systems, whether socialist or capitalist. Examples of general economic laws are the laws of demand and supply.

Uses of economic laws

Economic laws have the following uses:

(a) Economic laws are useful guides to economic events and serve as a basis for the formulation and evaluation of economic policies. For example the law of demand which states that the lower the price of a commodity the greater the quantity demanded can help the tax authority to fix a rate of tax that will not cause a big increase in price that will cause a big fall in demand.

(b) They are also useful in planning process. Planners can forecast implications of various plans by using economic laws. For example, what will happen to production when domestic industries are given subsidies.

(c) They are concerned with how the economic system work and operates. Man in his economic life produces wealth, consumes wealth and exchanges it with others. Therefore, economic laws govern production, consumption and exchange.

(d) Economic laws are also concerned with how the national product should be produced is distributed and how the levels of income and employment are determined.

(e) They establish relationship between cause and effect. Like laws of physical sciences economic laws also establish relationship between cause and effect about economic behaviour of man and economic phenomena. For example according to the law of demand when the price of a commodity falls its quantity demanded increases, other things remaining the same. Here the fall in price is the cause and the rise in the quantity demanded is the effect. The law of diminishing marginal utility describes that as a man has more units of commodity its marginal utility goes on diminishing. Here the increase in quantity demanded is the cause and the fall in marginal utility is the effect.

Ceteris Paribus

This is a Greek word which means other factors remain constant. Many economic laws apply under “Ceteris Paribus” conditions. For example the law of demand applies when other factors which determine demand like income, price of substitutes and weather remain constant. If these factors change when the price changes, the law will not apply.

For example, when the price decreases, the consumers will buy more if and only if income remains constant but when income also decreases, consumers will not be able to buy more even at a lower price.

Economy

Economy means using economic resources optimally, that is, using resources without wastage. Economy may also mean an economic system such as a capitalist system or a socialist system.

Welfare

Welfare refers to the level of satisfaction that a person or a group of persons derives from consumption of goods and services.

ECONOMIC SYSTEMS

Meaning of economic system

An economic system is a set of institutions within which a community decides on what, how and for whom to produce. It is a framework through which a society allocates scarce resources among competing uses or it is an allocative mechanism of a society. Thus, a society’s economic system determines how the society answers the fundamental economic questions about what should be produced. How the output is to be produced? Who to get this output etc.

Types of Economic Systems

There are three main types of economic systems:-

1. Command/Socialist economic system.

2. Capitalist economic system.

3. Mixed economic system.

Command or socialist economic system

A command or socialist economic system is a type of economic system in which all major means of production are owned by the state and all decisions about what, how, how much, where and for whom to produce are made by a central planning authority. Examples of countries, which practice this type of economic system, include the former U.S.S.R, China, Cuba and North Korea.

Features of Socialist Economy

A socialist economy has the following features:

- Collective ownership: Under the command system major means of production such as factories, banks, schools, hospitals, farms etc are owned by the state.

- All economic decisions are made by the state: Under the command systems all economic decisions of what should be produced, how to produce, for whom to produce are made by the central planning authority-The government is responsible for allocation of economic resources and distribution of wealth.

- Exploitation is minimized and classes are non-existent: Under the command system profit is shared equally among members of the society and classes do not exist since the wealth of the society is owned equally by all the members of the society and the motive of production is not to maximize profit. Therefore, there is no need to exploit workers by paying them low wages in order to make profit.

- Lack of competition and low growth: Socialist production is characterized by lack of competition and low growth of the economy. This is because production is carried by few monopoly government enterprises which do not compete to maximize output and profit. This renders them less efficient and generally leads to low growth of socialist economy.

- Lack of freedom of choice: In the command economy producers are not free to decide on the allocation of scarce resources, what should be produced is wholly determined by the state on behalf of all the people, consumers likewise are not free to decide on what goods to consume.

- Equality exists among the members of the society: In the command economy majority of the people have access to the national output as the state insures equal distribution of wealth among the citizens as a result every member of the society can obtain a minimum standard of living. Even the poor member of the society can still enjoy free social services that are provided freely by the government.

- Wasteful competition is avoided: In the command economy, production is carried out by few government owned Enterprises. These enterprises do not compete for allocation of resources because their major motive is not to maximize profit; they produce to satisfy the needs of the society. Due to lack of competition and proper planning by the government the problem of misuse of resources is often avoided.

- Lack of political freedom: A command economy usually operates under one party system. The party controls all socio-political and economic matters of the country, all citizens regardless of their differences in political opinions are forced to follow orders of the socialist party and freedom of expression is largely restricted.

- Bureaucracy in decision making and corruption: In the command system, the process of decision making is centralized and usually is made by a group of planners who undergo so many processes of decision making by estimating needs of the society. This process is very cumbersome since it involves so many procedures and is time consuming. The planners in one way or other control resources which make them liable for possible bribes from the consumers who are forced to use bribe in order to get scarce but essential commodities.

Advantages of Socialist Economy

A socialist economy has the following features:

- Equality: Under this system equality exists among the members of the society because everything is shared equally among members of the society. The government distributes wealth of the society or the national cake equally to the citizens.

- Lack of classes and exploitation: The major means of production are owned communally so there are no classes among the people in terms of ownership of major means of production. Exploitation is also minimized because no one in the society has control over the labour of another person, as it is the case in a capitalist economy, in which the capitalist exploits workers by paying them low wages.

- Promotion of majority welfare: Under this system the government ensures achievement of minimum standard of living for every member of the society by using different approaches like provision of free social services to all members of the society.

- Wastage of resources is avoided: Under command economy proper planning in the allocation of resources is done to ensure efficient and full utilization of resources and production according to the actual needs of the people. This avoids problems, which result from lack of planning such as overproduction, unemployment and the resulting price fluctuations.

- Control of individual monopolies: The government under command economy controls emergence of monopoly firms which often cause hardships to consumers and society like environmental pollution, charging extremely high prices and production of substandard goods.

- Economic and social crises can be avoided: Since the command economy is planned, the government is able to control various macro-economic variables like money supply, investment, consumption, expenditure, tax etc. In doing so, economic crises such as deflation, recession, depression and unemployment can be avoided. For example, the government may solve the problem of deflation through planning by reducing over investment.

Disadvantages of (command) socialist economy A socialist economy has the following features:

- Lack of freedom of choice: Under the command system the freedom of consumers and producers of what to consume and produce respectively are very limited. The government decides on behalf of all the people on what should be produced and consumed.

- Low motivation for producing and maximize profit: There is little motivation for producing by producers because the final output does not directly benefit them.

- Inefficiency in production: This system is characterized by inefficiency due to lack of competition, low technology, bureaucratic decisions, corruption, poor planning, too much protectionism policy to domestic industries etc.

- Lack of private initiatives: Public ownership discourages individuals to initiate various economic activities, innovate new methods of production, take risks in production etc.

- Absence of political freedom: People are forced to be members of one political party and restricted from forming civil society associations in order to express their views. Opposition parties are not allowed to operate in a socialist economy.

- Many officials of the government are required to estimate wants and direct resources: The use of such officials may lead to bureaucracy, excessive form filling, slowness in decision making and corruption.

- Resource mismanagement due to poor allocation: Often the government in a socialist state uses a lot of resources to consolidate political power instead of directing such resources to the production of economic goods.

- Slow investment and slow growth of output per worker: This is due to poor technological level caused by lack of motivation in carrying out some innovations among the people. Individuals have narrow chance to participate in the investment process since everything is government centered. This system has even made the people to become unable to raise enough capital for investment. Hence a decline in economic progress and in standard of living.

- Wastage is often overlooked and eventually turning government firms into loss making firms: This loss is usually borne by tax-payers or rate-payers.

- Difficult in estimating demand: It requires price signals to estimate existing and future pattern of demand for goods and services, in a command economy, planners often fail to know the actual demand for the people as a result shortages and wastage occur.

- Lags in implementation of plans: There is a time lag between the collection of information and the formulation of production plans based upon that information, and then there is a further time lag between the implementation of production and realization of production targets.

Nationalization Policy under a Socialist Economy

In order to build an effective command economy, most socialist governments nationalize private owned firms, that is, change private owned firms into public ownership.

Reasons for nationalization of firms/industries

- To regulate the production of demerit goods: The government may apply nationalization policy as a way of controlling demerit goods that is goods which are harmful to the consumers such as tobacco, gambling and beer.

- Fiscal reasons: The government may decide to nationalize private monopolies for a simple reason of using monopoly profit as a source of state revenue.

- To regulate production of merit goods and ensure public health: These are the public goods that are consumed by all the citizens such as water and electricity, the government control the supply of these commodities to ensure certain standards of these services so as to protect the welfare of the people.

- Defense and national security: For the sake of protecting national defense and security a government may nationalize the production of arms because if the production of the arms is under private firms, these firms may sell the arms even to the enemies of the country and jeopardize the security of the nation.

- National prestige: The government may nationalize some firms for a nation’s prestige. For example many governments possess and have national airlines in order to “wave the flag” of the country.