Regional Exams

Regional Exams COLUMNAR PETTY CASH BOOK

Topic Objectives.

By the end of this sub-topic, the student should be able to:

a) Describe the meaning of Two Column Cash Book

b) Discuss the need for Two Column Cash Book

c) Prepare a Two Column Cash Book

d) Account for treatment of contra entries

e) Explain the meaning of Three Column Cash Book

f) Prepare a Three Column Cash Book

g) Record cash discounts

h) Explain the concept of Petty Cash Book and imprest system

i) Record the petty expenditures in the Petty Cash Book

j) Use imprest system in recording petty cash transactions

The petty cash book is a further extension of the cash book. This book is used to record small payments or minor expenses such as postage fee, bus fare, stationery and entertainment. These minor expenses can make the normal cash book look bulky. A clerk called petty cashier is given the duty to write the petty cash book.

Advantages of having a petty cash book

To keep some of the minor details out of the cash book.

To reduce postings to the expense account.

To enable petty cash to be kept by someone other than the main cashier.

It provides an additional check as the petty cashier is not authorised to make payment without a voucher.

The money in the hands of the petty cashier is limited to the imprest amount hence misappropriation is made difficult.

How the petty cashier makes a payment

When a petty cashier makes a payment to a person, then that person will have to fill in a voucher showing exactly what the payment was for. Usually, the petty cashier will require evidence. In such a case, receipts or bills are presented. The recipients would sign the voucher to certify that their expenses have been offset by the petty cashier.

Meaning and application of the imprest system

Meaning of imprest system

It is a system where a refund of the total paid out in a period is made.

Application of the imprest system

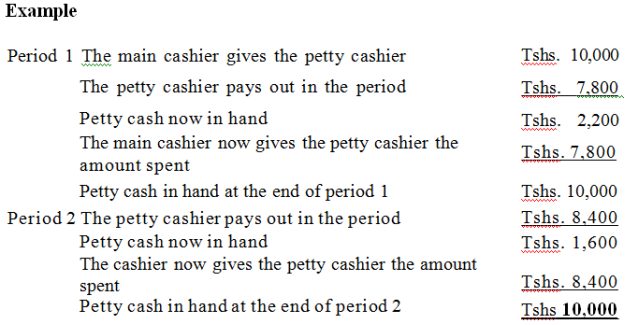

The main cashier gives the petty cashier enough cash to meet his or her needs for the following period called cash float. At the end of the period, the cashier finds out the amount spent by the petty cashier and gives him or her an amount equal to that spent.

The petty cashier will produce the petty cash vouchers as evidence of the amount spent. The petty cash in hand should then be equal to the original amount when the period was started.

It may be necessary to increase the fixed sum (often called the cash float) to be held at the start of each period. In the above case. If we had wanted to increase the float at the end of the second period to Tshs. 12,000, then the main cashier would have given the petty cashier an extra of Tshs. 2,000, that is 8,400 + 2,000 = 10,400.

Presentation of the petty cash book

The format of the petty cash book has both the debit and credit sides. However, the debit side is narrow than the credit side. The main column on the debit side is the amount column.

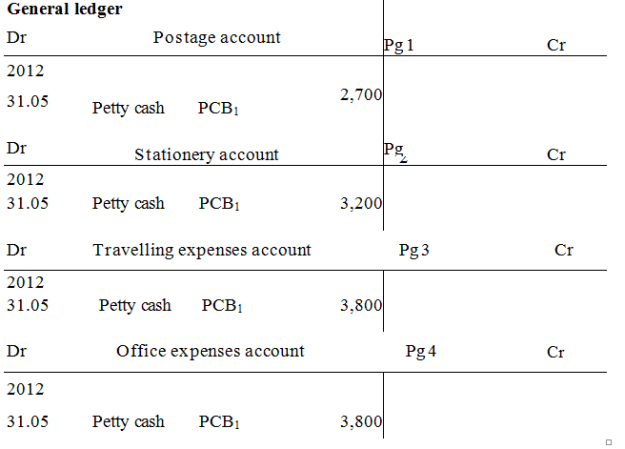

The number of columns on the credit side vary as they depend on the specific entities as outlined in the questions. For instance, we can have columns for postage, travelling, stationery and office expenses.

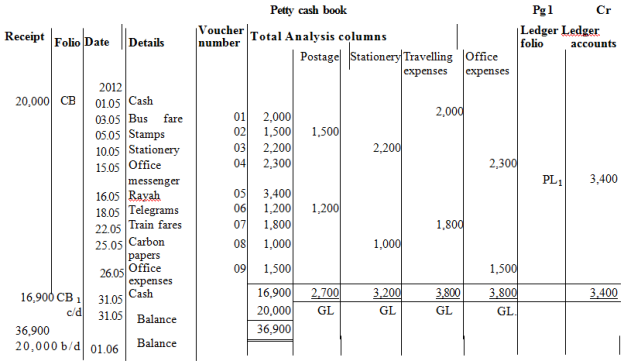

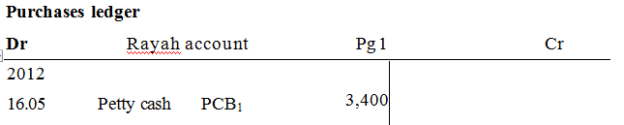

Format of a columnar petty cash book

Examples

1. Enter the following transactions in Bollas petty cash book having analysis columns for postage, stationery, travelling expenses, office expenses and ledger accounts.

Balance the petty cash book on 31.05.2012 bringing down the balance on 9.06.2012.

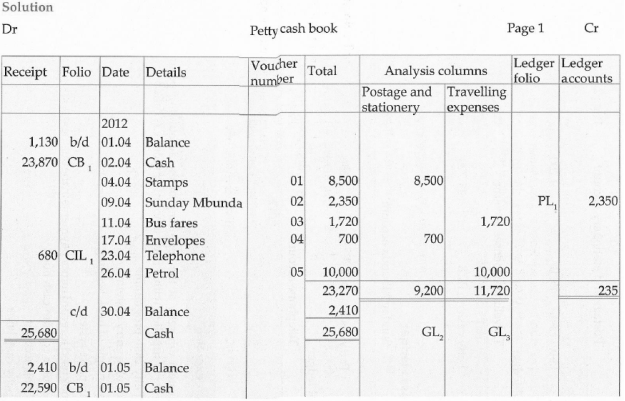

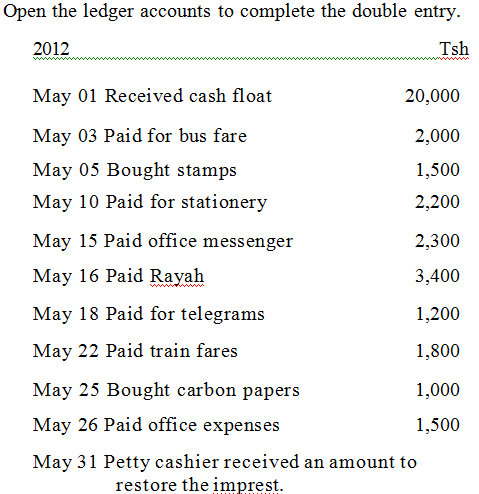

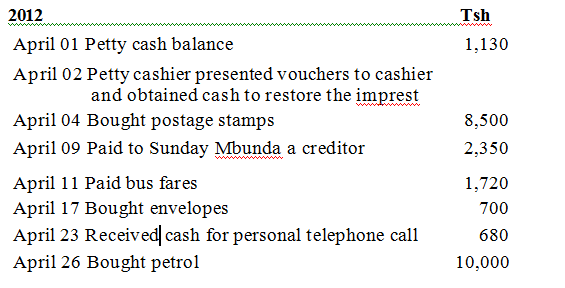

2. John Mary keeps her petty cash book on the imprest system. The imprest being Tshs. 25,000. For the month of April 2012, her petty cash transactions were as follows.

Required:

a) Enter the above transactions in the petty cash book on 30th April, bringing down the balance on May 1.

b) On 01.05, Mary received an amount of cash from the cashier to restore the imprest. Enter this transaction in the petty cash book.

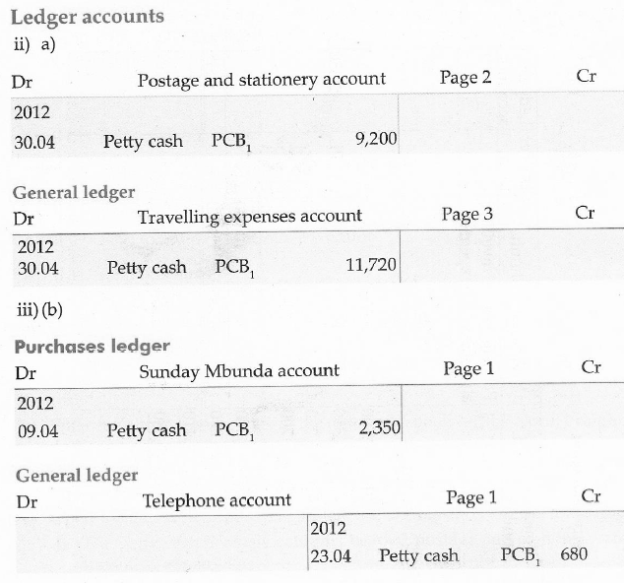

c) Open the ledger accounts to complete the double entry for the following:

i) The petty cash analysis columns headed postage and stationery and travelling expenses.

ii) The transactions dated 9th and 23rd April 2012.